Cash Stuffing in 2026: How TikTok’s Favourite Budget Method Looks on a Phone

By

Emma Carter

26.05.2026

12 min

Cash stuffing has gone from a niche personal finance trick to one of the most recognisable budgeting movements on the internet. With over 1.9 billion views under the #cashstuffing hashtag on TikTok, the cash stuffing method has clearly struck a chord with younger generations looking for a hands-on way to control their spending. But in 2026, most of our money never touches paper. So what happens when a budgeting system built on physical cash meets a world of tap-to-pay, subscriptions, and cross-border transfers?

This article traces how cash stuffing digital budgeting actually works today: from the original envelope method your grandparents might recognise, through the TikTok-era cash stuffing revival, to the modern digital envelope budgeting tools and multi-wallet systems that solve the problems cash never could. We’ll look at what makes the method effective, where it falls apart, and how a multi wallet app with real sub-balances and optional cards changes the equation entirely.

Where Cash Stuffing Came From — and Why TikTok Brought It Back

The idea behind cash stuffing is older than most people realise. Long before the term existed on social media, households across Europe and America were dividing their income into labelled envelopes: one for rent, one for groceries, one for savings. Personal finance educator

Dave Ramsey popularised the technique in the early 2000s through his “Financial Peace University” programme, calling it the envelope system. The principle was straightforward: when the envelope is empty, you stop spending in that category. No exceptions.

What changed in the 2020s was the format. Beginning around 2021, creators on TikTok — many of them young women navigating their finances for the first time — started filming themselves dividing cash into colour-coded binders and transparent pouches. The aesthetic was part of the appeal: watching neatly sorted banknotes go into labelled sleeves was oddly satisfying, almost meditative. The hashtag #cashstuffing surged past a billion views by 2023, and by 2025 the trend had spawned its own micro-economy of binder accessories, custom dividers, and even full-time content businesses. One TikTok creator, Jasmine Taylor, built a cash stuffing accessories and courses business that reportedly brought in $2.2 million in 2024.

The timing wasn’t accidental. Cash stuffing TikTok exploded during a period of rising inflation and growing consumer debt. Gen Z shoppers were found to make nearly double the number of impulse purchases compared to older demographics, heavily driven by social media exposure. A

Bank of America study found that over half of Gen Z adults do not have enough emergency savings to cover three months of expenses. Against that backdrop, a budgeting method that physically prevents you from overspending had obvious appeal.

The Psychology: Why Physical Limits Work Against Impulse Spending

The cash stuffing method works not because it’s clever, but because it’s painful — in a useful way. Research consistently shows that people spend less when they pay with physical cash compared to cards. MIT economist Drazen Prelec demonstrated that credit cards increase consumers’ willingness to pay because the transaction feels abstract.

Swiping or tapping a card doesn’t trigger the same psychological friction as handing over banknotes.

Cash stuffing takes this insight and builds a system around it. When you assign €200 to your “groceries” envelope and you can see the stack of notes thinning by Wednesday, you make different decisions. You skip the impulse snack aisle. You check what’s already in the fridge before heading to the shop. The method doesn’t just track spending — it creates a hard ceiling.

This is exactly what makes envelope budgeting different from most budgeting apps that merely log transactions after the fact. The spending limit isn’t a notification you can dismiss. It’s an empty envelope you can’t refill until the next payday.

For a generation dealing with the compounding pressure of social media advertising, in-app purchasing, and one-click checkouts, that friction is genuinely valuable. Survey data from Credit Karma found that roughly three-quarters of Gen Z are aware of cash stuffing and about a third actively use some form of it.

Where Cash Envelopes Break Down in a Digital World

For all its psychological power, the traditional cash stuffing system has real blind spots — and they get worse every year as Europe moves further away from cash-based spending.

You can’t pay online with an envelope

Subscriptions, online shopping, utility bills on direct debit — none of these accept cash. For anyone managing rent, streaming services, insurance, or freelance software tools, a purely cash-based system leaves out most of the monthly budget. You end up running a parallel system: envelopes for groceries and coffee, a card for everything else. The discipline splits, and so does the visibility.

Security and access

Keeping hundreds of euros in cash at home carries obvious risks: theft, fire, accidental loss. UK insurer data has consistently flagged this concern in relation to the cash stuffing trend. And if you’re travelling, carrying a set of labelled envelopes through airports isn’t exactly practical.

No cross-border flexibility

For Europeans who live in one country and earn or spend in another — freelancers, remote workers, expats — cash-only budgeting simply doesn’t scale. SEPA transfers, multi-currency needs, and international invoicing all happen digitally.

Cash Stuffing: What It Solves vs. Where It Breaks

| What it solves | Where it breaks |

|---|---|

| Stops impulse spending through physical limits | Cannot be used for online purchases or subscriptions |

| Creates visual awareness of remaining budget | Cash at home is vulnerable to theft or loss |

| Simple: no apps, no logins, no learning curve | No cashback, no rewards, no return on idle money |

| Forces pre-planning before each pay cycle | Doesn’t scale for freelancers or cross-border finances |

| Emotionally connects you to spending | Requires regular ATM visits and manual tracking |

Digital Envelope Budgeting: From Paper to Pixels

Digital envelope budgeting takes the core principle — divide your money into purpose-labelled containers and only spend from the right one — and moves it into software. Instead of stuffing paper envelopes, you assign money into virtual envelopes that live inside an app.

There are broadly two categories of digital envelope tools in 2026:

Standalone budgeting apps

Apps like Goodbudget, YNAB (You Need A Budget), EveryDollar, and several newer envelope budgeting app options let you create virtual envelopes and manually log transactions. These are tracking layers — they help you see where your money is going, but they don’t actually hold or move money. You still need a separate payment account and card. The budget exists in the app; the money exists in your account. And the two aren’t always in sync.

These tools work well for people who are disciplined about manual entry. Goodbudget’s free tier, for instance, allows limited envelopes and two devices, while the premium version unlocks unlimited envelopes and bank-account syncing. YNAB charges $14.99 per month (or $109 annually) and is built around zero-based budgeting principles. EveryDollar, designed by Ramsey Solutions, relaunched in early 2026 with new features including a “margin finder” and coaching tools.

The limitation is that these apps only inform your decisions — they don’t enforce them. If your “Dining Out” envelope in Goodbudget shows €0 remaining, nothing stops you from swiping your card at a restaurant anyway.

Sub-accounts inside financial apps

Several European fintech platforms now offer pockets, vaults, or spaces — sub-balances within a single account that you can label and allocate money to. These are closer to the original envelope concept because the money is actually separated, not just tagged in a tracker.

However, there are common constraints. Sub-accounts are often locked behind paid tiers. Many don’t allow you to attach a separate card to each pocket, which means you still spend from a single main balance and manually reconcile. And few offer genuine per-wallet features like individual IBAN-level separation or independent transaction histories.

The gap between these two approaches — trackers that don’t hold money and sub-accounts that can’t spend independently — is exactly where a true

multi wallet budgeting system becomes relevant.

Multi-Wallet Budgeting: When Your Envelope Is Also a Payment Method

The reason cash stuffing works is that each envelope is both a budget container and a spending instrument. You don’t track your grocery spend — you pay from the grocery envelope. The budget and the payment are the same thing.

That’s exactly the logic behind budgeting with multiple wallets inside a financial app — but without the limitations of physical cash. A genuine multi-wallet system lets you create separate euro wallets for different purposes: one for rent, one for groceries, one for travel, one you don’t touch. Money moves between wallets instantly. And the key difference: you can optionally link a separate card to each wallet, so that when you pay, you’re spending directly from that specific budget — not from a general balance.

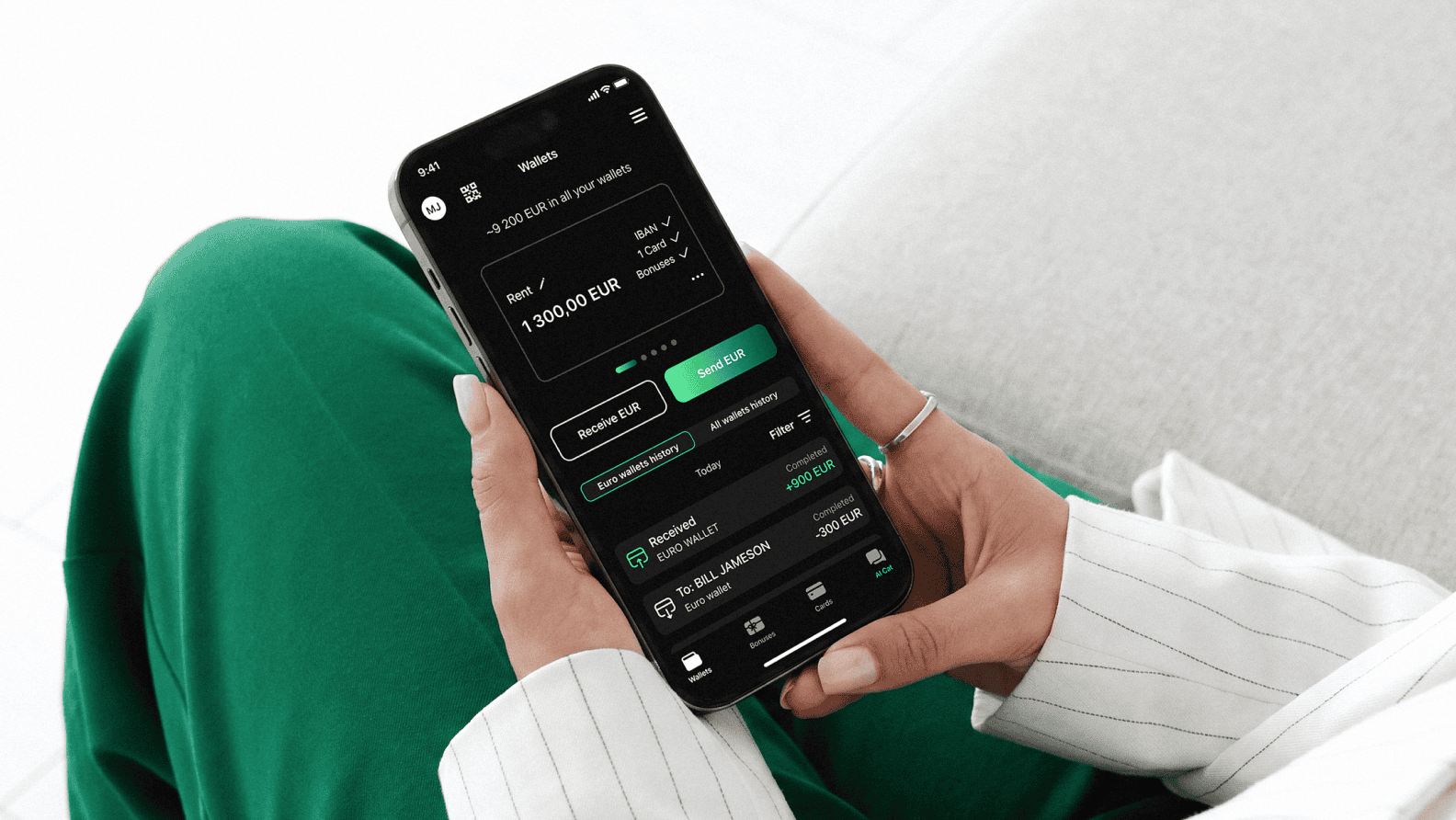

This is the model available through the Blackcat app. Users can create multiple euro wallets inside the same account, each with its own balance and transaction history. Wallets can exist with or without a linked card. Creating wallets is free. If you add one or more additional cards, a single €2 monthly fee applies regardless of how many extra cards you have.

Here’s what that looks like in practice:

Example: a freelance designer in Berlin

Lena earns €3,200 per month from client invoices, all landing in her main Blackcat fiat wallet. Before she touches anything, she moves €960 into a "Tax Reserve" wallet — roughly 30% of her gross income, set aside for quarterly tax payments and health insurance contributions. The remaining €2,240 gets split across four wallets:

- "Rent & Bills" — €1,000, no card. Money sits here and goes out via SEPA transfers to her landlord and utilities.

- "Daily Life" — €550, with a linked card. This is what she taps at the supermarket, café, and pharmacy. When it's low, she sees it before she spends.

- "Fun Money" — €150, with a linked card. Restaurants, concerts, spontaneous weekend plans. When it hits zero, she's done for the month.

- "Don't Touch" — €300, no card. Her emergency cushion. She moves money in and forgets about it.

- "Tax Reserve" — €960, no card. Untouchable until her quarterly Vorauszahlung is due. This is the wallet most freelancers wish they'd had from day one.

Lena’s setup mirrors the classic cash stuffing method, but everything works digitally: she pays online, receives SEPA transfers, sees her balances in real time, and doesn’t need to visit an ATM. She also has the option to activate a bonus programme in the app — such as a 4% p.a. reward on her account balance, paid monthly in euros, without locking any funds.

The bonus payment is a part of the loyalty program provided by Baltic Technology Solutions OÜ. Detailed terms and conditions can be found at

Comparing the Three Approaches: Cash, Apps, and Multi-Wallet

Not every budgeting method suits every person. Below is a side-by-side view of how the three main envelope-style approaches compare across the features that matter most.

| Feature | Cash Envelopes | Budgeting Apps (e.g. Goodbudget, YNAB) | Multi-Wallet with Cards |

|---|---|---|---|

| Money actually separated | Yes — physically | No — tracking layer only | Yes — separate wallet balances |

| Spend enforcement | Hard limit (empty = done) | Soft — alerts only | Hard limit per wallet |

| Works for online payments | No | Tracks them, but doesn’t enforce | Yes — card linked per wallet |

| Cashback / rewards possible | No | Depends on linked account | Yes, if provider offers them |

| Setup cost | Free (envelopes) | Free tier or €8–15/month | Free wallets; €2/mo for extra cards |

| Cross-border / SEPA | No | No (tracking only) | Yes |

| Best for | Low-spend, cash-heavy lifestyles | Budget-aware planners | Freelancers, multi-goal savers, digital spenders |

How to Set Up Your Own Digital Envelope System

Whether you use a dedicated cash stuffing app, a budgeting tool, or a multi-wallet financial app, the setup process follows the same logic the method has always used. Here’s how to build your system from scratch.

Step 1: List your spending categories

Go through your last two to three months of transactions. Group every expense into a category. Be honest about where money actually goes, not where you wish it went. Most people land on five to eight categories. Common ones: housing and bills, groceries, transport, personal spending, dining and social, subscriptions, taxes and savings or emergency fund.

Step 2: Set a realistic limit per category

Based on your actual spending history, assign a euro amount to each category. If you’ve been spending €400 on groceries and you think you can do €350, start there. Don’t set aspirational numbers that you’ll blow through by week two — that’s how people abandon budgets entirely.

Step 3: Choose your tools

Decide whether you need a tracking-only app, a sub-account system, or a full multi-wallet setup. If most of your spending is digital, the tracking-only approach will require more discipline since nothing actually prevents overspending. A

multi wallet app where you can link a card to each wallet gives you the digital equivalent of a hard-stop envelope.

Step 4: Allocate on payday

When income arrives, immediately distribute it into your wallets or envelopes. This is the digital equivalent of a cash stuffing session. Some apps allow automatic distribution rules; in the Blackcat app, you move money between wallets manually, which preserves that deliberate, hands-on quality that makes the method work.

Step 5: Spend only from the right wallet

If you’ve linked cards to wallets, use the right card for the right purpose. Groceries go on the groceries card. Restaurants go on the fun card. When a wallet runs low, you see it in real time — and you make the same gut-check decisions you’d make staring at a thinning stack of banknotes.

Step 6: Review and adjust monthly

At the end of each month, look at which wallets had money left over and which ran out early. Adjust your allocations. Redirect surpluses towards savings or debt repayment. The system is only as useful as your willingness to fine-tune it.

Three Scenarios Where Digital Envelopes Outperform Cash

The subscription trap

You sign up for a streaming service, a fitness app, a cloud storage plan, and a news subscription. Individually, each costs under €15. Together, they’re draining €50–70 per month. Cash envelopes can’t catch this because subscriptions don’t use cash. But a dedicated “Subscriptions” wallet with a linked card makes the total spend visible. If you’ve only allocated €40 and the wallet is running dry, you know which subscription to cancel.

Splitting finances with a partner

Two people sharing expenses can create a joint wallet for shared costs — rent, groceries, household items — while keeping individual wallets for personal spending. No more guesswork about who owes what. Each person tops up the shared wallet by an agreed amount each month. The wallet’s transaction history is the receipt.

Saving for a specific goal

Cash stuffing fans often create envelopes for goals: a holiday, a new laptop, an emergency fund. The digital version is a wallet with no card attached. Money goes in but doesn’t come out easily. Unlike a paper envelope, the balance is tracked precisely, it’s protected by the security of your financial app, and it doesn’t lose purchasing power sitting in a binder. If your provider offers a balance-based reward, the money can even grow while it waits.

What to Look for in a Digital Envelope Tool

If you’re evaluating which approach fits your financial life, here are the features worth checking before committing:

| Feature | Why it matters |

|---|---|

| Separate wallet balances (not just labels) | Ensures your budget is actually enforced, not just tracked |

| Optional card per wallet | Lets you spend directly from a specific budget — the digital equivalent of pulling cash from an envelope |

| Free wallet creation | You shouldn’t pay to create categories. Budgeting complexity varies; your tool should accommodate it |

| SEPA transfer support | Paying rent, bills, or invoices from specific wallets keeps the system complete |

| Bonus or reward programmes | Money allocated to savings or buffer wallets should ideally not sit idle |

| No mandatory paid tier for basic features | The core envelope system should work on a free plan |

| Real-time balance visibility | Replaces the visual check of looking into a cash envelope |

The Blackcat app checks these boxes:

free wallet with card creation, SEPA transfers from any wallet, optional cards linked to individual wallets, and access to bonus programmes including a 4% p.a. reward on account balance — all available without a paid subscription. You can explore the full wallet functionality at

blackcat.app/wallet.

Summary: Cash Stuffing Isn’t Dead — It Just Moved to Your Phone

The principle behind envelope budgeting — give every euro a job before you spend it, and stop when the allocation runs out — is as sound in 2026 as it was in 1996. What’s changed is the infrastructure. Physical cash can’t keep up with the way most Europeans pay, save, and transfer money today.

Digital envelope budgeting preserves the discipline while removing the friction. And the most effective version of it isn’t a tracking app that logs spending after the fact — it’s a system where the budget and the payment method are the same thing. Separate wallets, each with its own balance and optional card, recreate the tangible feeling of cash stuffing without any of its limitations.

Whether you’re a Gen Z budgeter who discovered cash stuffing on TikTok or someone who’s been filing banknotes into envelopes for years, the upgrade path is the same: keep the mindset, change the medium.

FAQ

What is cash stuffing and why is it popular?

Cash stuffing is a budgeting method where you withdraw cash and physically divide it into labelled envelopes for different spending categories. It became hugely popular on TikTok between 2021 and 2025 because it creates a visual, tactile way to manage money that resonates with younger generations struggling with impulse spending. The method works by making spending feel real — when the cash in an envelope is gone, spending stops.

How does envelope budgeting work?

Envelope budgeting works by assigning a fixed amount of money to each spending category (groceries, entertainment, transport, etc.) at the beginning of a pay cycle. You spend only from the relevant envelope. If the groceries envelope is empty by Wednesday, you cook from what’s in the cupboard rather than going shopping. The method forces pre-planning and prevents overspending because the physical limit is absolute.

What is digital envelope budgeting?

Digital envelope budgeting applies the same principle using apps or financial platforms instead of physical cash. Some tools, like Goodbudget or YNAB, create virtual envelopes that track your spending but don’t hold actual money. More advanced solutions use real sub-balances or multiple wallets inside a single account, where money is genuinely separated and can be spent using linked cards — replicating the hard-stop limit of a cash envelope in a fully digital environment.

Can I do cash stuffing without physical cash?

Yes. The core idea — pre-allocating money to specific purposes and refusing to overspend — doesn’t require paper currency. A multi wallet app that lets you create separate wallets with individual balances and optional linked cards achieves the same result digitally, while also supporting online payments, subscriptions, and cross-border transfers that cash cannot handle.

What are the limitations of cash stuffing?

The main limitations are: you cannot use cash for online purchases or subscriptions; keeping large amounts of cash at home creates security risks; cash doesn’t earn any return; and the method doesn’t work well for people who manage finances across borders or need to make SEPA transfers. Manual tracking is also required since there’s no automatic transaction history.

How do multi-wallet apps improve budgeting?

Multi-wallet apps improve on both cash envelopes and tracking-only budgeting apps by combining budget separation with actual payment functionality. Each wallet holds real money, can have its own linked card, and supports digital transactions including SEPA transfers. This means your budget categories are also your spending instruments — the same principle that makes cash stuffing effective, but compatible with the way most people actually pay for things in 2026.

Share this article