Contactless Payments in Europe: How They Work and What Limits to Know

By

Emma Carter

18.05.2026

10 min

You tap your card, the terminal beeps, and you walk away with your coffee. The whole thing takes about two seconds — and yet behind that casual gesture sits a surprisingly sophisticated system that has reshaped how an entire continent pays for things.

The latest

ECB payments statistics for H1 2025 put the numbers into perspective: 29.6 billion contactless card payments were made in the euro area in just six months, up 12.8% year-on-year. The total value hit €0.8 trillion. At the end of H1 2025, 93% of all point-of-sale terminals in the eurozone accepted contactless transactions, and the average euro area inhabitant held 2.5 payment cards.

The contactless payments Europe relies on every day aren't the future — they're the default. But how exactly do they work? What are the contactless payment limits across Europe? When does your PIN kick in? And how do Apple Pay, Google Pay, and virtual cards fit into the picture? Let's unpack it.

How Do Contactless Payments Work?

Every contactless card payment — whether from a plastic card,

virtual card, phone, or a smartwatch — relies on NFC (Near Field Communication). Your card or device contains a tiny antenna and a secure chip. When you hold it within a few centimetres of a payment terminal, the two devices exchange encrypted data almost instantly. The terminal reads your payment credentials, confirms the amount, and sends an authorisation request to your card issuer. If approved, the payment is done. No PIN. No signature.

What makes this secure is that the chip generates a unique, one-time cryptographic code for each transaction. Contactless cards produce what the industry calls a dynamic CVV (iCVV) — a code that's valid only for that single payment. Even if someone physically intercepted the NFC signal (they'd need to be within 4 centimetres), the captured code would be useless for anything else.

NFC payments Europe-wide have been growing rapidly. The

ECB's H2 2024 data showed 29.5 billion contactless transactions worth €0.8 trillion in that half-year alone — a 15.5% increase over the same period in 2023. Card payments now account for 57% of all non-cash transactions in the euro area, and contactless is the dominant mode within that.

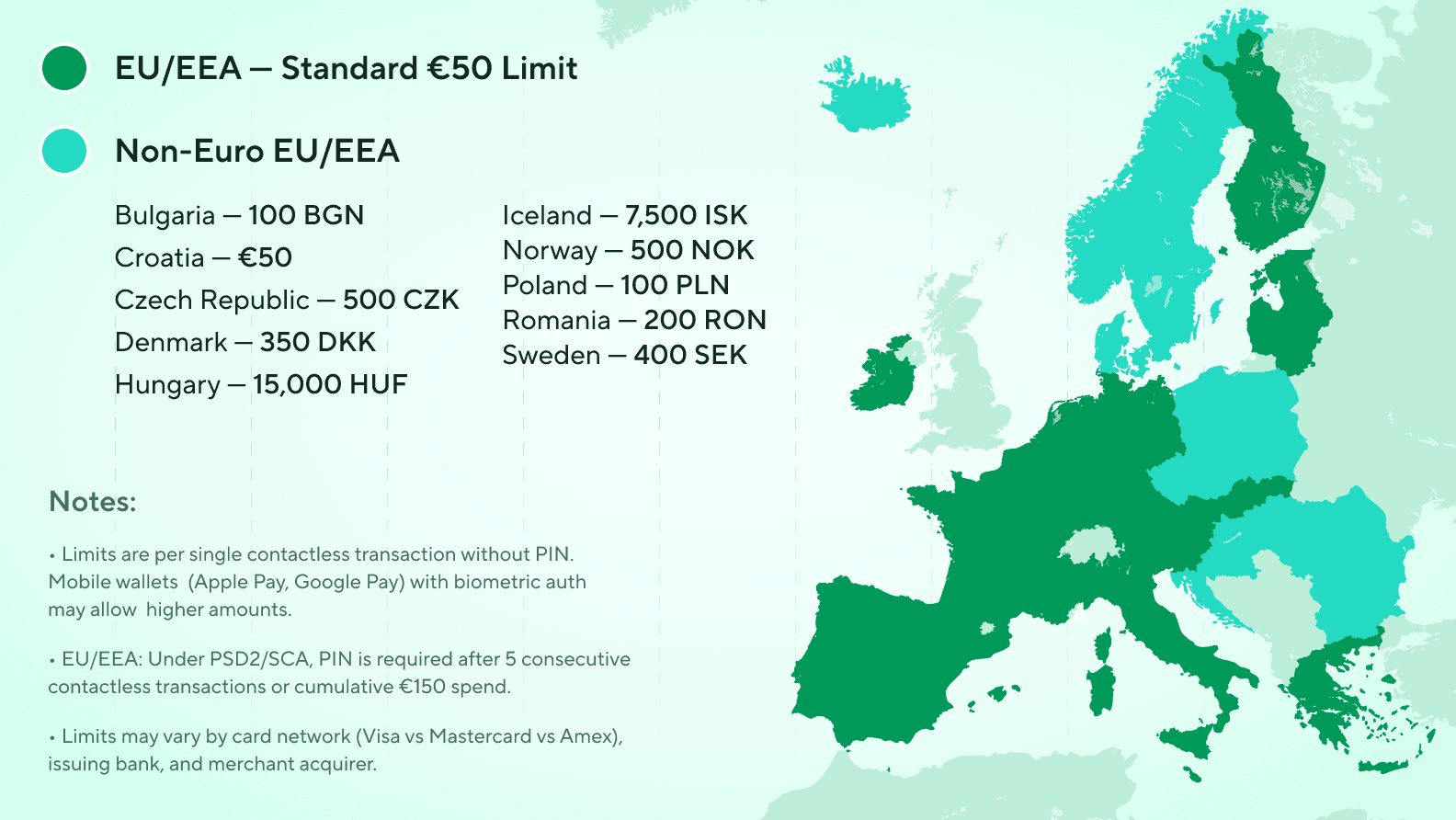

What Is the Contactless Payment Limit in Europe?

The number you'll encounter most often across the eurozone is €50 per transaction. This is the maximum individual contactless payment that can be processed without PIN authentication, as specified in

Article 11 of the Commission Delegated Regulation (EU) 2018/389 — the regulatory technical standards on Strong Customer Authentication (SCA) under PSD2.

The €50 cap applies in the vast majority of eurozone countries, including Germany, France, Spain, Italy, the Netherlands, Austria, Belgium, Ireland, Portugal, Greece, Malta, and the Baltics. According to the

European Commission's PSD2 overview, these limits are part of the SCA exemption framework designed to balance convenience with fraud protection.

But the eurozone standard is only part of the picture. Non-euro European countries set their own limits, and the variation is significant. Based on

Merchant Machine's 2026 data and

FF News reporting:

| Country | Contactless Payment Limit | Approximate EUR Equivalent |

|---|---|---|

| Germany, France, Spain, Italy, Netherlands, Austria, Ireland, Malta | €50 | €50 |

| Poland | 50 PLN | ~€12 |

| Czech Republic | 500 CZK | ~€20 |

| Sweden | 400 SEK | ~€35 |

| Hungary | 15,000 HUF | €38 |

| Romania | 200 RON | ~€40 |

| Switzerland | 80 CHF | ~€82 |

| UK | £100 | ~€117 |

Poland's limit at roughly €12 is one of the lowest in Europe. The UK's £100 is the highest — and from March 2026 the UK is removing its fixed national cap, allowing individual providers to set their own contactless limits.

A

2021 survey by Payments Europe of 3,200+ consumers across France, Germany, Italy, Spain, Sweden, and Poland found that the majority would actually be comfortable with limits up to €150 — three times the current cap. Consumer appetite is ahead of regulation.

When Do I Need to Enter a PIN for Contactless Payments?

Even when your individual transaction is under the €50 limit, you'll periodically be asked for your PIN. This isn't a glitch — it's a security feature mandated by PSD2.

According to the

EBA's official Q&A (2018/4225), the rules work as follows. Your card issuer must apply SCA (i.e., request your PIN) when either of these thresholds is hit:

- The cumulative total of consecutive contactless transactions since the last PIN entry exceeds €150, or

- The number of consecutive contactless transactions since the last PIN reaches 5

This means you might be asked for your PIN on a €3 coffee if it's your sixth consecutive tap. Or on a €45 purchase if your cumulative total has just crossed €150. It's predictable once you understand the system — and it's an important layer of protection if your

contactless payment card is lost or stolen.

How Do Apple Pay and Google Pay Work with Payment Cards?

This is where tap to pay Europe-wide gets interesting for people who want to go beyond the €50 limit.

When you use Apple Pay or Google Pay, you're adding an extra authentication layer — biometric (Face ID, fingerprint) or a device PIN — before the NFC signal leaves your phone. Because you've already verified your identity on the device, the transaction is treated as SCA-authenticated by many issuers. This means the €50 per-transaction cap that applies to a physical card often does not apply to mobile wallet payments.

In practice: you might be limited to €50 when tapping your plastic card at a supermarket in Berlin, but could pay €150+ with your phone at the same terminal. The merchant's terminal just sees an authenticated contactless payment.

This is one of the strongest practical reasons to add your

payment card to a mobile wallet. Blackcat cards can be added to

Apple Pay directly in the app. If you regularly make purchases above the €50 physical card limit — a full grocery shop, a restaurant bill, a last-minute hotel — tapping your phone removes that friction entirely.

Google Pay works the same way from a technical standpoint. You add your card to the Google Wallet app, verify it, and use tap to pay at any NFC-enabled terminal. The biometric or device-lock authentication means higher limits and no cumulative PIN triggers. Both Apple Pay Europe users and Google Pay Europe users benefit from this approach equally — the authentication happens on your device, not at the terminal.

Can Virtual Cards Be Used for Contactless Payments?

Yes — and this is a point many people miss. A

virtual card isn't limited to online purchases.

Once you add a virtual card to Apple Pay or Google Pay, it works exactly like a plastic card at any NFC terminal. You tap your phone, the payment goes through. A virtual card contactless payment looks identical to a plastic card tap from the terminal's perspective. What it receives is a tokenised, encrypted payment credential — the same format regardless of card type.

This means you can open a

Blackcat account, receive a virtual card instantly (no waiting for postal delivery), add it to your mobile wallet, and start making contactless payments at physical shops within minutes.

Where it gets really useful is in combination with a

multi-wallet system. Blackcat lets you create unlimited wallets, each with its own IBAN and optional virtual card. You can issue a separate contactless-enabled virtual card for each wallet — one for daily spending, one for travel, one for subscriptions — and tap to pay from whichever wallet you choose. Every wallet runs a

bonus program.

Are Contactless Payments Safe for Everyday Spending?

Short answer: yes, and the data supports this strongly.

Contactless card payments are protected by multiple layers. First, the NFC chip generates a unique one-time code per transaction, so intercepted data is useless. Second, the €50 single-transaction cap and the €150/5-transaction cumulative limit mean that even a stolen card has a built-in ceiling on damage. Third, PSD2 caps cardholder liability at a maximum of €50 in the case of unauthorised transactions (and zero if the loss wasn't detectable), as outlined by the

European Commission.

On top of regulatory protection, modern payment providers add their own layers.

Blackcat's security features include PCI DSS compliance for card data handling, 3D Secure authentication for online payments, ISO 27001-aligned information security, instant freeze to block a card immediately from the app, and custom spending limits per card.

The ECB's own data shows that card fraud rates in the euro area have been declining even as contactless volumes surge — a strong signal that the security architecture is holding up.

Can Contactless Payments Be Used Abroad in Europe?

Absolutely. Your contactless payment card works anywhere in Europe that accepts the same card network (Mastercard, Visa) — which is essentially everywhere. The NFC protocol is standardised, so a card that works in Amsterdam will work in Lisbon, Warsaw, or Zurich.

The main thing to watch when travelling is the local contactless limit. If you're used to tapping freely in Germany at €50, you'll find that Poland's 50 PLN (~€12) limit means your PIN is needed much sooner. Conversely, if you cross into Switzerland (80 CHF, ~€82) or the UK (£100), you have more headroom.

This is another reason why linking your card to Apple Pay or Google Pay before travelling is smart — the biometric authentication often overrides local physical-card limits, giving you consistent behaviour across borders.

With a

Blackcat payment card, your account is EUR-based with a

European IBAN. SEPA transfers work across the EEA, UK, and Switzerland, and your card is accepted at any Mastercard-accepting terminal worldwide. Free incoming SEPA transfers and

5 free outgoing SEPA transfers per month keep cross-border costs predictable.

What Should I Do If a Contactless Payment Is Declined?

A contactless decline at the terminal usually has one of four causes:

1 . You've hit the cumulative SCA limit. Either five consecutive taps or €150 in cumulative contactless spend. Solution: insert your card and enter your PIN. The counter resets.

2 . The amount exceeds the local contactless limit. The purchase is above €50 (or the local equivalent). Solution: use chip-and-PIN, or pay with your phone via Apple Pay/Google Pay (which may support higher limits).

3 . Insufficient funds. Your account balance doesn't cover the purchase. Solution: top up your

wallet — via SEPA, internal transfer from another wallet, or crypto-to-EUR conversion if you use Blackcat's integrated crypto service.

4 . Technical issue. The terminal, your card's chip, or the NFC connection had a momentary problem. Solution: try again, try a different terminal, or insert the card manually.

If the decline seems wrong — your balance is sufficient and you haven't hit any limits — check your payment app for real-time transaction alerts. With Blackcat, every transaction triggers an instant push notification, and you can verify your balance, freeze cards, or adjust limits directly in the

app.

Practical Tips for Contactless Payments in Europe

Know the limits before you travel. The table above is your cheat sheet. Poland, Czech Republic, and Sweden have lower limits than the eurozone standard.

Add your card to Apple Pay or Google Pay. This is the single most useful thing you can do for everyday contactless spending — higher limits, biometric security, and your phone is always in your pocket. Blackcat makes this easy with

Apple Pay integration directly in the app.

Carry your plastic card as backup. Some merchants, ATMs, and rural areas still don't support NFC. A physical card in your wallet covers you when technology doesn't cooperate.

Use a wallet with card setup for budgeting. Assign different virtual cards to different wallets — daily spending, travel, entertainment — and tap to pay from the right one. You'll always know which pool of money you're spending from.

Enable real-time notifications. Don't wait for a monthly statement to spot something wrong. Instant alerts from your payment provider mean you can act in seconds.

The Bottom Line

Contactless payments in Europe are fast, secure, and increasingly the default. The per-transaction limit in most eurozone countries is €50, but mobile wallet payments through Apple Pay and Google Pay often bypass this cap. Cumulative PSD2 triggers (€150 or 5 transactions) mean your PIN will be requested periodically regardless. And virtual cards work identically to plastic ones when added to a mobile wallet — meaning you can start tapping the day you open an account.

Understanding these mechanics doesn't just save you from awkward moments at a checkout. It helps you use your money more confidently, whether you're buying a flat white in Vienna or paying for a week's groceries in Warsaw.

FAQ: Contactless Payments in Europe

How do contactless payments work?

Contactless payments use NFC (Near Field Communication) technology. Your card or phone exchanges encrypted data with a payment terminal when held within a few centimetres. The chip generates a unique one-time code for each transaction, and the payment is authorised by your card issuer in under a second. No PIN or signature is needed for transactions within the local limit.

What is the contactless payment limit Europe applies to tap transactions?

In most eurozone countries — including Germany, France, Spain, Italy, the Netherlands, and Austria — the limit is €50 per transaction. Non-eurozone countries set their own limits: the UK allows £100, Switzerland 80 CHF (€82), while Poland caps it at 50 PLN (€12). These limits apply to physical card taps; mobile wallets like Apple Pay may allow higher amounts due to built-in biometric authentication.

When do I need to enter a PIN for contactless payments?

Yes — do contactless payments require PIN entry? They do, periodically. Under PSD2, your card issuer must request your PIN after either five consecutive contactless transactions or when your cumulative contactless spend reaches €150 — whichever threshold the issuer applies. Once PIN is entered, the counter resets. This applies even if every individual transaction was well below €50.

Can I use a virtual card for contactless payments?

Yes — can virtual cards be used for contactless payments just like plastic ones? Absolutely. Once a virtual card is added to Apple Pay or Google Pay, it functions identically to a physical card at NFC terminals. The terminal receives a tokenised payment credential and cannot distinguish between a virtual and a plastic card. This means you can start making contactless payments the same day you open an account and receive your virtual card.

Can I use Apple Pay for contactless payments?

Yes. You add your payment card to the Apple Wallet app, verify it through your card issuer, and then hold your phone near any NFC terminal to pay. The phone uses biometric authentication (Face ID, fingerprint) or a device PIN before transmitting the payment, which is why many issuers allow higher transaction limits than physical cards. Blackcat cards can be added to Apple Pay directly in the app.

Can I use Google Pay for contactless payments?

Yes. Google Pay works the same way as Apple Pay for contactless transactions. You add your payment card to the Google Wallet app, verify it through your card issuer, and hold your phone near any NFC terminal. The device-lock or biometric authentication means many issuers treat the transaction as SCA-compliant, often allowing higher limits than a physical card tap.

What happens above contactless limit?

If your purchase exceeds the local contactless limit (€50 in most eurozone countries), the terminal will decline the tap and ask you to insert your card and enter your PIN instead. Alternatively, you can pay using Apple Pay or Google Pay on your phone, which often supports higher limits thanks to built-in biometric authentication. The same PIN requirement applies when your cumulative contactless spend hits €150 or you reach five consecutive taps.

Are contactless payments safe for everyday spending?

Yes. Each tap generates a unique cryptographic code that can't be reused. Transaction limits cap exposure if a card is stolen. PSD2 limits cardholder liability to €50 maximum for unauthorised transactions. And modern payment providers add further layers: real-time notifications, instant card freeze, 3D Secure for online payments, and PCI DSS compliance for data handling.

Can contactless payments be used abroad in Europe?

Yes. Any contactless payment card works at any NFC-enabled terminal across Europe, regardless of the country you're in. The card network (Mastercard, Visa) is standardised. The main variable is the local contactless limit — which varies by country — so check the limits for your destination. Adding your card to Apple Pay or Google Pay often bypasses local physical-card limits.

What should I do if a contactless payment is declined?

The most common causes are: you've hit the cumulative SCA limit (insert your card and enter PIN to reset), the purchase exceeds the local contactless limit (use chip-and-PIN or pay via phone), insufficient funds (top up your account), or a temporary technical issue (try again or use a different terminal). Check your payment app for real-time alerts to diagnose the issue quickly.

Share this article