Euro Card for Everyday Spending in Europe: What to Check

By

Emma Carter

22.06.2026

8 min

Most of us choose a card for reasons that have nothing to do with how it performs: the colour, a headline cashback number, the word free. Or follow our friends' choice. Then we find out what the card is really like at the worst possible moment — when it's declined at a counter, when a small fee shows up on an unexpected line of the statement, or when an online payment just won't go through. A good euro card for everyday spending in Europe isn't the one that looked best in the ad; it's the one that quietly handles all of that. This guide flips the order: here's what actually decides whether a euro card is any good, so you can check for it before you commit, not after.

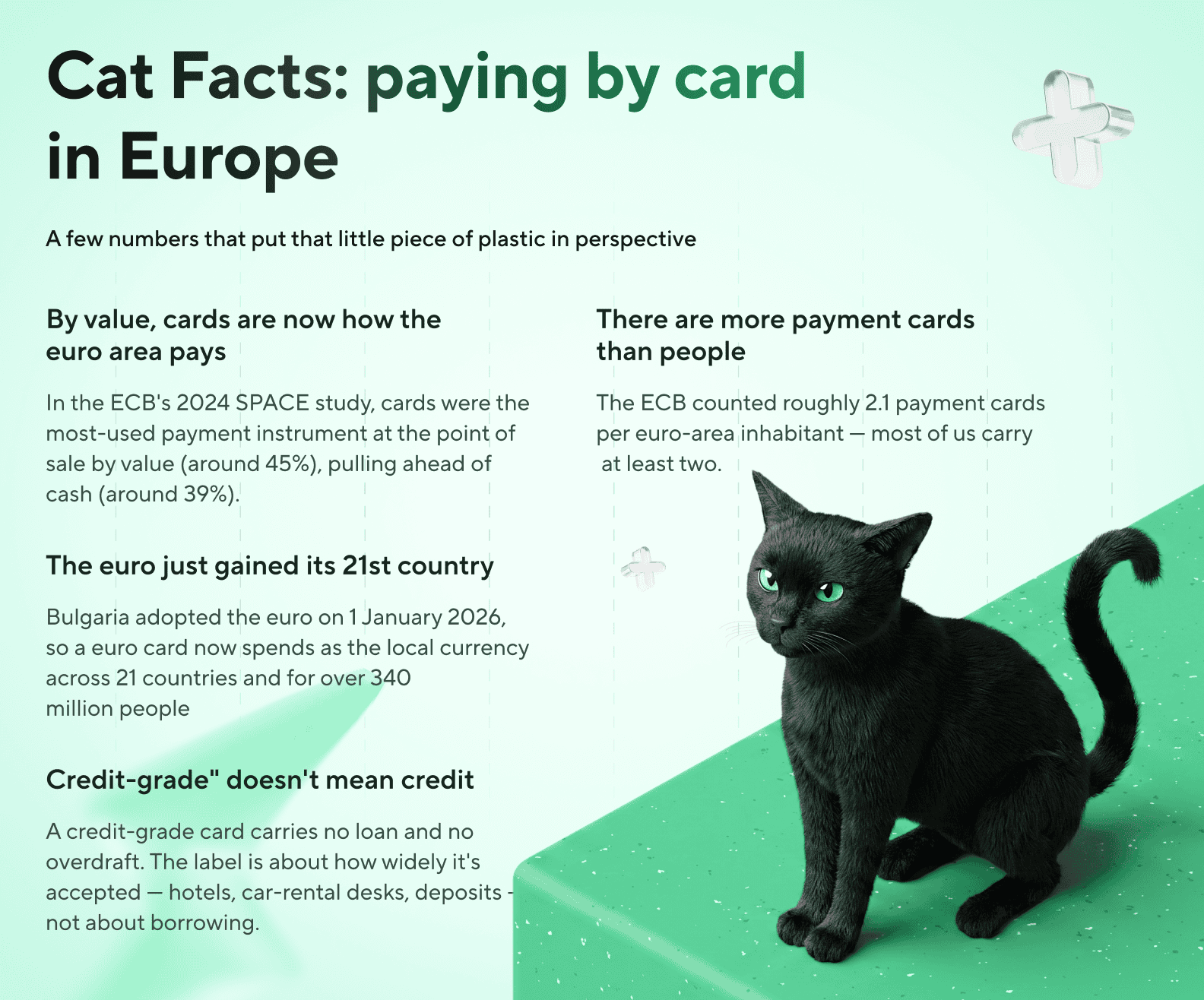

It's worth getting right, because the card does more work than you'd think. By value, cards are now the most-used way people pay at the till across the euro area, ahead of cash, according to the

ECB's 2024 SPACE study. A handful of small differences — where it's accepted, what it costs, how much control you get — show up every single day.

What a euro card actually is (and what it isn't)

So, what is a euro card? It's a payment card denominated in euros, tied to a euro payment account, that spends your own EUR balance — not a line of credit. There's no borrowing and no monthly bill to settle; an EUR payment card simply moves the euros you already have. When people ask how the euro payment card work, that's really the whole of it: you tap, insert, or enter the details, the amount leaves your balance, and the payment clears — whether it's a coffee, a supermarket run, or a checkout online. EUR card payments behave the same way everywhere.

The account underneath matters more than the plastic on top. Can a euro card be linked to an IBAN account? Yes — and ideally it is. With a payment card with IBAN access, the same euro balance can receive transfers (a salary, an invoice, a refund) and fund your spending in one place, instead of a top-up wallet you keep feeding.

Picture the IBAN account as the container and the card as the tool attached to it — the everyday form of a European payment card: euros in, euros out, usable across the continent.

The takeaway: a euro card is a spending instrument, so it should be judged on how it spends. That's exactly what the rest of this checklist does.

Where it'll actually be accepted

The first thing people skip when choosing is acceptance — and it's the first thing that bites. Almost any card pays for a coffee; the gap shows up at the awkward moments: hotel check-in, the car-rental desk, anywhere a deposit or pre-authorisation is placed. That's where some cards get declined, because the merchant needs to put a temporary hold on funds and not every card handles that well.

This is where the card's grade quietly matters. Although a euro card like this works as a prepaid-style card with no credit or overdraft, a credit-grade BIN means it's accepted in those situations where many other cards get rejected. Concretely: you land, pick up a hire car, and the desk pre-authorises €300 against the card as a deposit; with a credit-grade card that hold goes through, where a card without it can be turned away at the counter. So one real check is blunt — will it be accepted where it actually counts, not just at the supermarket? And can I use a euro card abroad more generally? Within the euro area — now 21 countries after

Bulgaria joined in 2026 — you're simply spending euros in a euro economy; outside it the card still works, though a conversion fee may apply, which is the next thing to check.

What it costs you

A card advertised as cheap can quietly become expensive, which is why fees are the check that pays you back. What fees should I check before using a euro card? Run down this short list:

- Account or monthly fee — is there a recurring charge just to hold the card and account?

- ATM withdrawals — fees and monthly free-withdrawal limits, which vary a lot between providers.

- Card issuance and delivery — whether ordering a plastic card or a replacement costs anything.

- Inactivity or dormancy fees — easy to miss, and annoying if the card sits unused.

The other side of cost is rewards. Some euro cards add a loyalty reward paid on your balance, or cashback on what you spend — fair to weigh, with two caveats: cashback typically applies only to card purchases (not ATM withdrawals, transfers, or top-ups), and any such reward sits inside a loyalty programme with its own terms, so read them rather than assume.

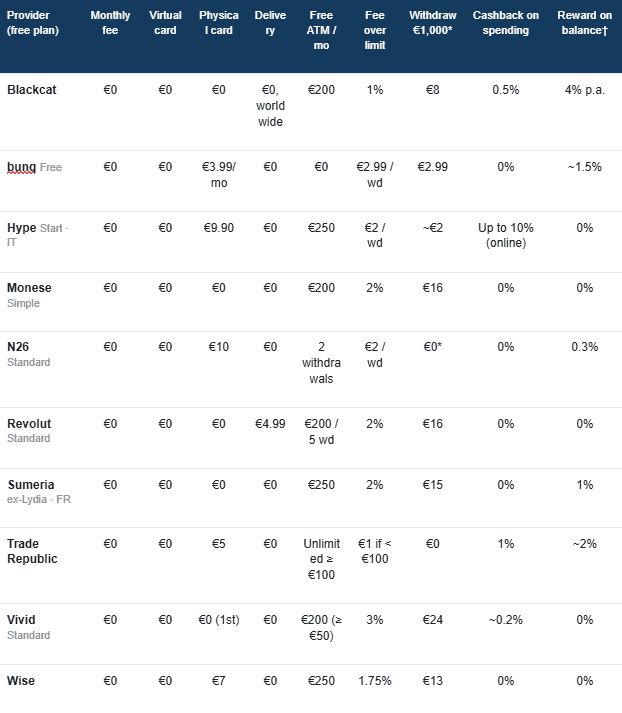

Free-tier euro cards in Europe, side by side

Plenty of euro cards advertise a free plan — but a "free" euro card can hide very different fees once you look closer. Here's how the free tiers of Europe's most popular euro cards compare on what they really cost: issuing a virtual or physical card, delivery, ATM withdrawals, and the rewards you earn back.

*Illustrative cost of a single €1,000 ATM withdrawal in one month. Amount-based plans charge a percentage on the part above the free limit; count-based plans (e.g. N26, Trade Republic) charge per withdrawal regardless of size, so one large withdrawal can look cheaper than several small ones.

†Reward/interest on balance is variable and usually condition-dependent (e.g. minimum card use, sub-account or savings product, balance caps) and changes often. Figures are headline rates as of the date below.

Data as of 16 June 2026

Terms change frequently and vary by country and region. Figures are taken from each provider's published fee pages; Blackcat figures from blackcat.app. Always check current terms before choosing.

Virtual vs plastic: which you actually need

People treat this as an either/or, and it isn't. What is the difference between virtual and plastic card options? A virtual euro card is just the card details — number, expiry, security code — created instantly in the app, ideal for online and in-app payments and for sites you don't fully trust. A plastic euro card is the physical one you tap or insert in shops and use at an ATM. Most people are best served by having both.

| Virtual card | Plastic card | |

|---|---|---|

| Best for | Online checkouts, subscriptions, in-app payments | In-person shops, contactless, ATM withdrawals |

| How fast you get it | Instantly in the app | Ordered and delivered |

| Risk control | Create or freeze per use; easy to replace | Freeze/limit in the app; replace if lost |

| Works abroad | Yes, online and in mobile wallets | Yes, in person and at ATMs |

Control, and what to do when something goes wrong

The last check is the one people only value after a problem: how much control the card gives you, and how it behaves when a payment fails. Good

card security features are practical, not decorative — freeze and unfreeze instantly, set or lower limits, switch online payments on and off, and spin up a virtual card for risky sites. Combined with the 3D Secure confirmation step, those advanced security measures keep you in charge of where and how the card is used, rather than hoping for the best.

And when a payment does bounce — it happens — the cause is usually mundane. What should I do if a euro card payment is declined? Work through the likely reasons in order: not enough balance for the amount (including any pre-authorisation hold, like a hotel or fuel station placing a temporary block); a daily or per-transaction limit you've set or hit; a 3D Secure step not completed or timed out; an expired or mistyped card detail; or the card simply frozen in the app. Checking your balance, limits and app status clears the large majority of declines. For

everyday EUR spending you can rely on, that everyday controllability is worth as much as any sign-up perk.

The short version

Choose by what the card does, not how it looks. Check where it's accepted (credit-grade for hotels, car rentals, deposits), what it really costs (FX markup, ATM fees, monthly charges), whether you get both a virtual and a plastic card, and how much control you have (freeze, limits, 3D Secure). Get those four right and you've checked what actually makes a payment card Europe-wide useful day to day — the colour stops mattering.

FAQ

What is a euro card?

A payment card denominated in euros and linked to a euro payment account, so it spends your own EUR balance. It works in shops, online, and at ATMs, with no credit or borrowing involved.

How does a euro payment card work?

You pay by contactless, chip, or by entering the card details online; the amount is taken from your euro balance and the payment clears. It draws on a payment account, not a credit line.

Can I use a euro card for online payments?

Yes. Almost all euro cards work for e-commerce, and you'll usually confirm with a 3D Secure step — a tap in the app or a one-time code. A virtual card adds extra safety for unfamiliar sites.

Can I use a euro card while travelling in Europe?

Yes. Within the 21 euro-area countries there's no conversion and no FX markup. Outside the euro area it still works, but a currency-conversion fee may apply, so check your provider's FX markup first.

What is the difference between a virtual card and a plastic card?

A virtual card is card details with no physical object, created instantly and ideal for online use. A plastic card is the physical card for in-person payments and ATMs. Most people use both.

Can a euro card be linked to an IBAN account?

Yes, and ideally it should be. A card backed by a real IBAN lets the same euro balance receive transfers (like a salary) and fund your spending in one place, rather than a wallet you keep topping up.

What fees should I check before using a euro card?

Account or monthly fees, FX markup for spending outside the euro area, ATM withdrawal fees and limits, card issuance and delivery costs, and any inactivity fees. These are where a "cheap" card can quietly turn expensive.

What should I do if my euro card payment is declined?

Check your balance (including any pre-authorisation hold), your limits, whether the 3D Secure step completed, the card details, and whether the card is frozen in the app. Those cover the large majority of declines.

This article is general information, not legal, tax or financial advice.

Share this article