Crypto Card For Freelancers: Why More Freelancers Are Quietly Switching From Bank Transfers

By

Hamna Zain

01.06.2026

11 min

Three freelancer friends told me the same thing in two weeks. A designer in Karachi. A developer in Buenos Aires. A copywriter in Lisbon. Different time zones, different work, same fix: they had stopped relying only on international bank transfers and were using app-based payment products to receive crypto income, convert it into fiat, and spend through ordinary payment rails.

The banks still got the rent. The groceries still went through a normal card terminal. But international invoices no longer had to pass through the slowest and most expensive part of the banking system.

This piece looks at what is happening on the ground with freelancer crypto payments. It explains what a crypto card usually is, why some freelancers are using crypto-enabled payment apps, how euro spending can work, where the cost savings appear, and what risks still matter.

Importantly, not every product works like a typical crypto card directly linked to a stablecoin wallet. Blackcat, for example, uses a different two-step model: the user can receive crypto through an integrated crypto service in the app, manually convert it into EUR, and then spend from a separate IBAN payment account using a fiat payment card. The card and the crypto feature are separate, independent parts of the workflow.

We will cover the SWIFT cost problem, the “country tax” caused by weak FX access, holding dollar or euro value without a traditional foreign bank account, everyday fiat card spending, cashback marketing, custody risk, tax events, and the checks freelancers should run before using a crypto-enabled payment product.

What a Crypto Card Actually Is

Strictly speaking, the thing in your hand is not magic. A cryptocurrency card is usually a prepaid or debit-style card connected to a crypto balance. The novelty is not the plastic card or the phone wallet. The novelty is how the balance is funded.

In a typical crypto-card model, the card connects to a wallet holding stablecoins or other digital assets. When the user taps to pay, the provider converts part of the crypto balance into fiat at or near the moment of authorization. The merchant receives euros, dollars, or another local currency. The merchant does not need to know that the source of funds was a digital-asset balance.

So the line that “you are spending crypto” is not quite right. In most cases, the user is selling crypto and spending fiat. That distinction matters because it affects fees, tax reporting, custody risk, and what happens if the provider freezes the account.

However, not every product works through a direct crypto-wallet-to-card model. Blackcat’s structure is different. The Blackcat card is not directly linked to a crypto wallet. Instead, the user can receive crypto through an integrated crypto service in the app, manually convert that crypto into EUR, and then use the EUR balance through an IBAN payment account and fiat payment card. In other words, the crypto feature and the payment-card feature are separate and independent.

This two-step structure can be an advantage for freelancers. It gives the user more control over when crypto is converted into EUR, keeps ordinary card spending in fiat, and avoids presenting the card as a product that directly spends crypto at the point of sale.

For freelancers, the appeal is simple: they may be able to receive value from international clients faster than some bank routes, convert it into EUR when needed, and then spend from a fiat payment account using a normal payment card. This makes the product better understood as a crypto-to-EUR-to-card workflow, rather than a traditional crypto card directly linked to a wallet.

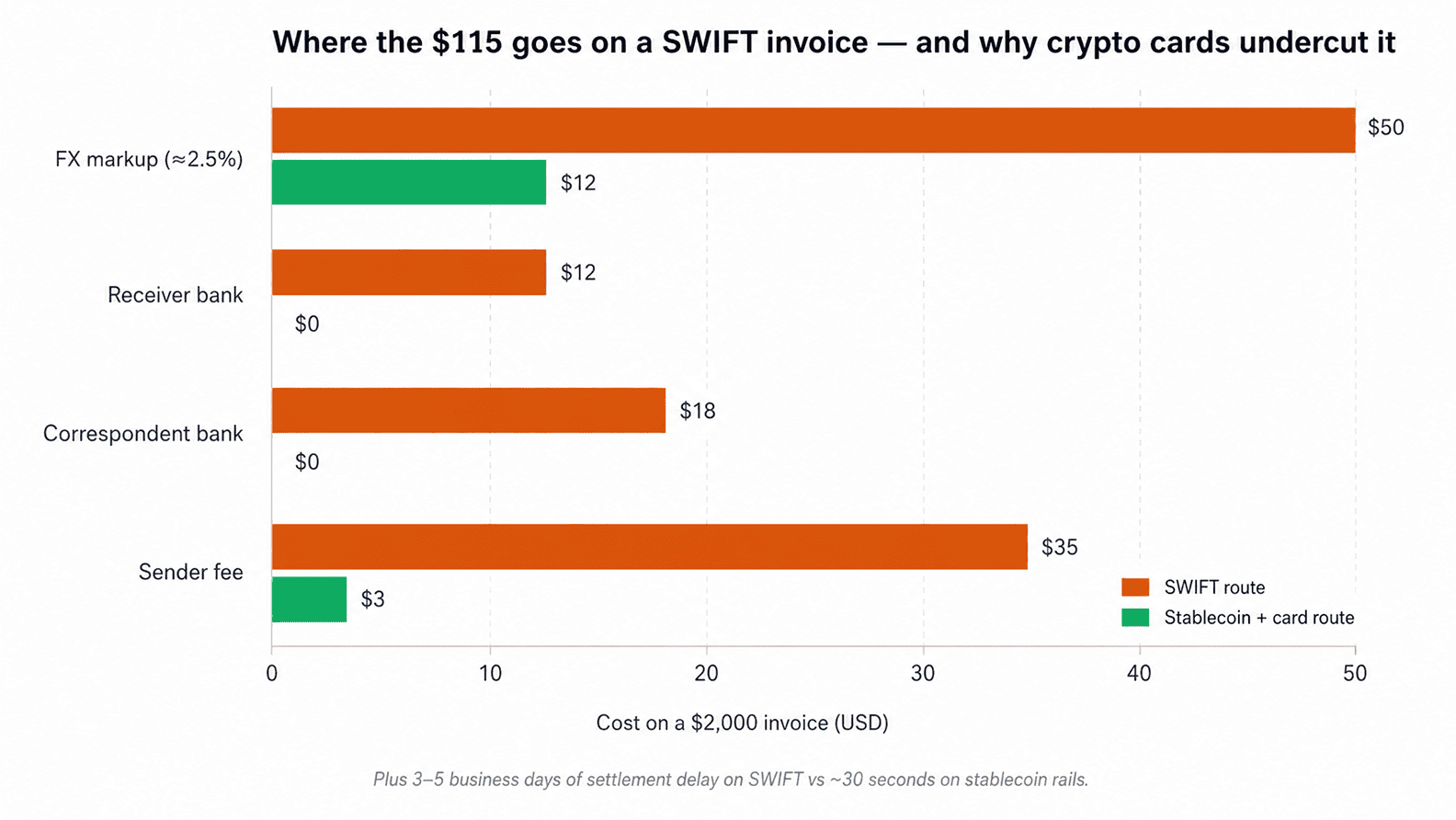

Story 1: The SWIFT Problem

For many freelancers, getting paid internationally is not just about earning in dollars. It is about how long those dollars take to arrive, how much is deducted along the way, and whether the freelancer can predict the final amount.

A typical SWIFT payment may pass through intermediary banks before reaching the freelancer’s local account. Each intermediary can deduct a fee. The receiving bank may also charge an incoming transfer fee. In some cases, payments are delayed because of compliance checks, missing payment references, or correspondent banking issues.

This creates a cash-flow problem. A freelancer may invoice $2,000 but receive less than expected several days later, without a clear breakdown of where the deductions happened. For small businesses and independent workers, that uncertainty matters.

Stablecoin payments can solve part of this problem by making settlement faster and more transparent. The freelancer can receive a dollar-linked asset directly, then decide when and how to convert or spend it. This is not risk-free. Stablecoins depend on the issuer, the blockchain network, the wallet provider, and local rules. But compared with waiting several days for a bank transfer with unclear deductions, the appeal is obvious.

This is why searches around crypto card Europe, crypto to euro card, and can freelancers avoid international transfer delays are increasing. Many freelancers are not trying to speculate on crypto. They are trying to get paid faster, keep more control over their money, and spend across borders with fewer delays.

Caption:

Estimated cost and timing breakdown of a typical $2,000 SWIFT invoice versus a stablecoin route. Actual costs vary by bank, country, provider, and compliance requirements.

Estimated cost breakdown of a typical $2,000 SWIFT invoice versus a stablecoin route, based on author's review of freelancer corridors. Actual costs vary by bank, country, and provider.

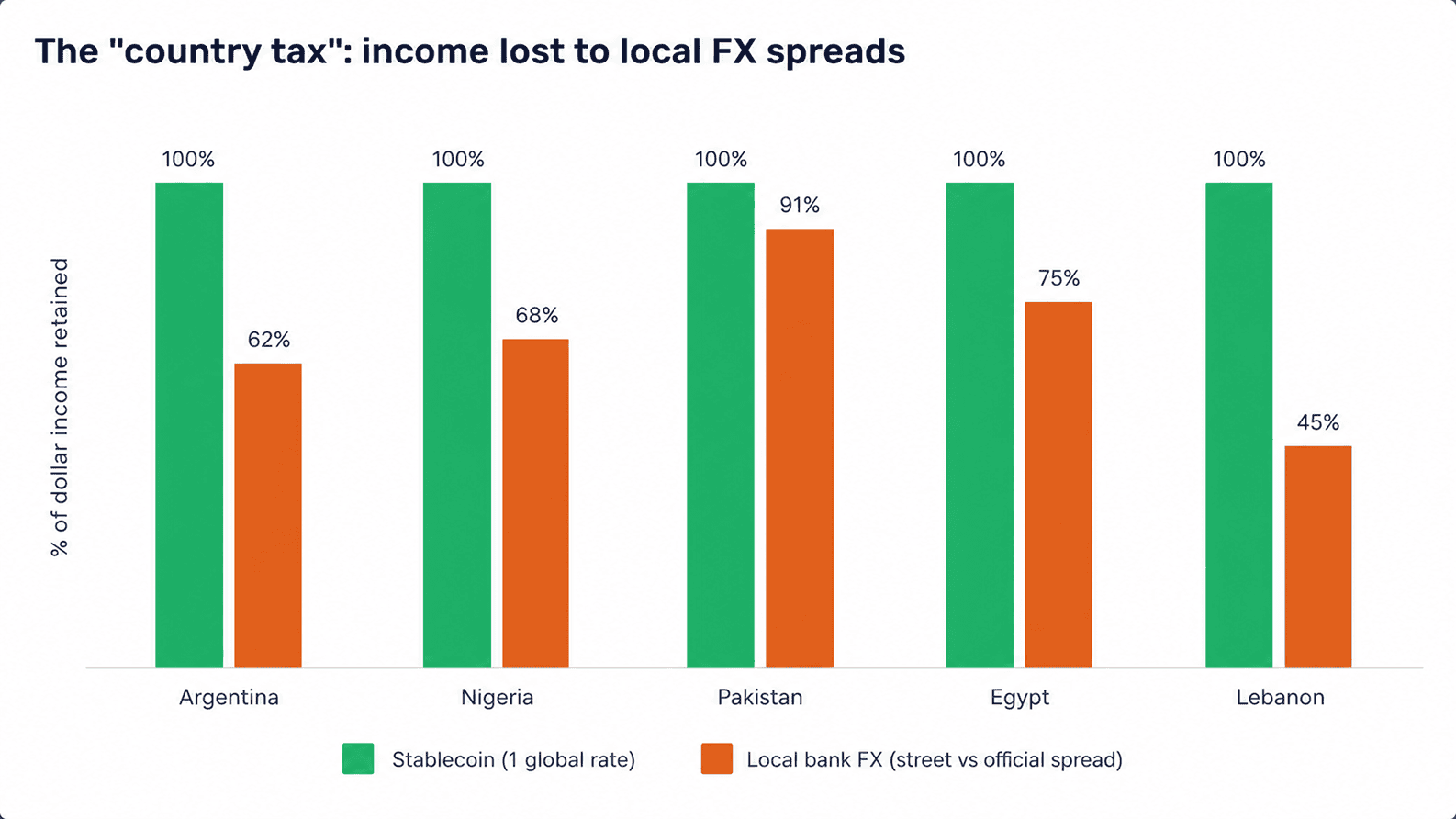

Story 2: The Country Tax

Some countries quietly tax freelancers through the FX system. Not always officially, and not always through a line item on a statement. The cost appears when a freelancer earns in dollars but receives money through a formal banking channel at a weaker conversion rate than the market rate they actually live with.

This is why if freelancers can avoid international transfer delays is only half the question. The other half is whether they can avoid unnecessary FX leakage.

In some corridors, a crypto card can reduce part of that loss. Stablecoins often function as digital dollars, and the freelancer converts only when spending. That is not risk-free. Stablecoins can trade at small premiums or discounts, and local rules may restrict access. But for some freelancers, the ability to hold value closer to dollars until the point of purchase is the main reason they switch.

This is also where crypto card Europe and crypto to euro card searches come from. A freelancer may receive a dollar-linked stablecoin, travel or live in Europe, and want to spend in EUR without waiting for a bank transfer to clear.

Illustrative comparison of the share of dollar income retained under formal banking FX versus a stablecoin route in five emerging-market corridors. Figures are indicative; actual rates fluctuate.

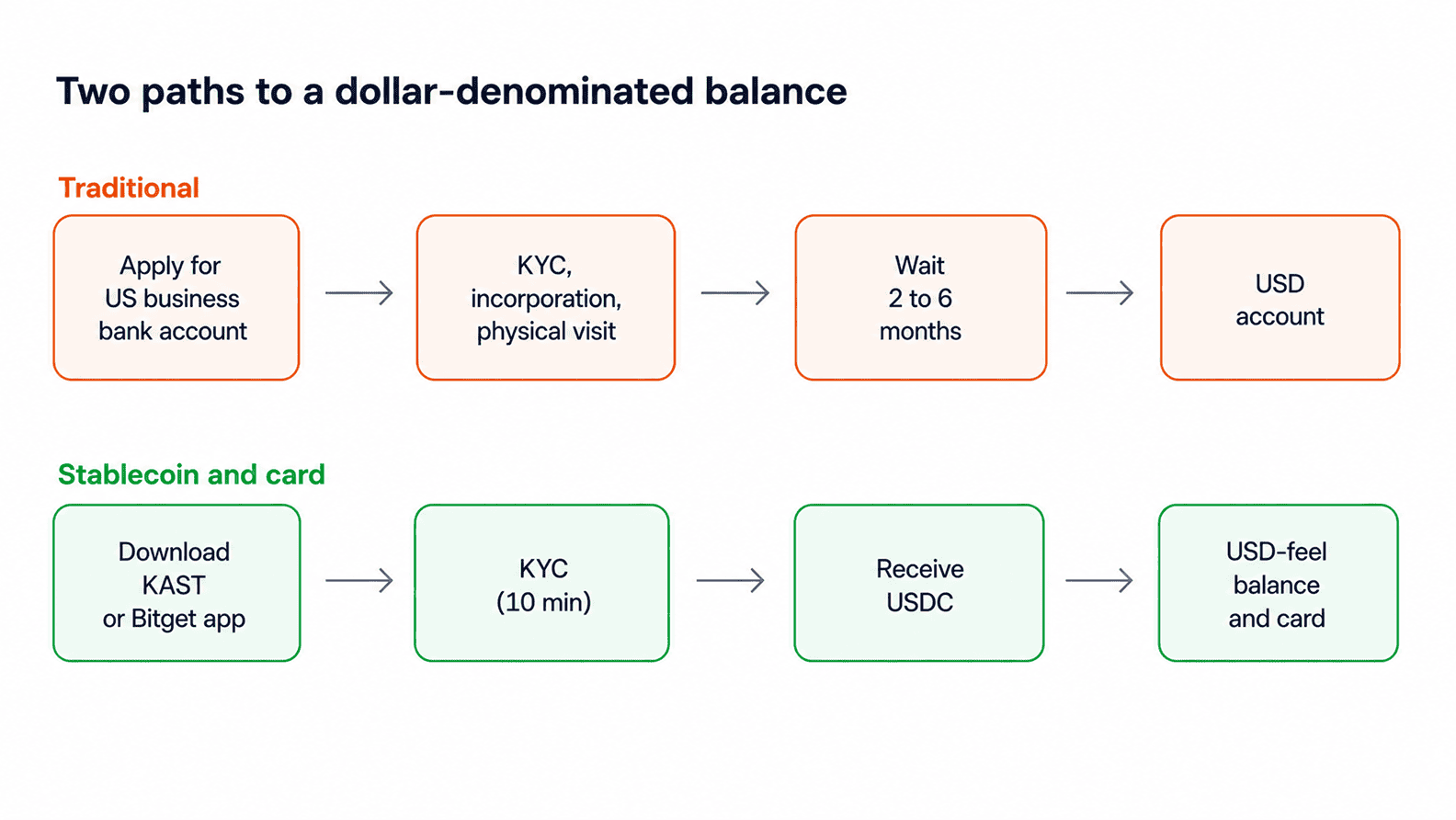

Story 3: A Dollar Balance Without a Foreign Bank Account

A lot of freelancers want a dollar or euro balance without spending months trying to open a foreign bank account remotely. A stablecoin balance can sometimes fill that gap quickly, and a crypto-enabled payment app can make international income easier to manage for ordinary expenses.

In a typical crypto wallet with card model, a freelancer may receive USDC, keep it in a wallet, and use a card to pay for software subscriptions, flights, groceries, or client-related expenses. In Europe, this is often marketed as a crypto to euro card, because the user receives crypto income and spends euros through a payment card.

But not every product works in exactly the same way. Blackcat’s model is different from a typical crypto card directly linked to a crypto wallet. With Blackcat, the user can receive crypto through an integrated crypto service in the app, manually convert that crypto into EUR, and then use the EUR balance through an IBAN payment account and fiat payment card.

This separation matters. The Blackcat card is not spending crypto directly at the point of sale. The user first converts crypto into EUR, and the card then spends fiat from the payment account. For freelancers, this two-step structure can be useful because it gives more control over when conversion happens, keeps everyday card spending in fiat, and makes the product easier to understand as a crypto-to-EUR-to-card workflow.

This does not mean the product is the same as a bank account. The legal treatment, tax treatment, deposit protection, complaint rights, and regulatory coverage can be very different. Freelancers should still check fees, conversion spreads, custody, transaction records, and local rules before relying on any crypto-enabled payment product.

The two paths to a dollar-denominated balance for a non-US freelancer. Timelines vary by jurisdiction and provider.

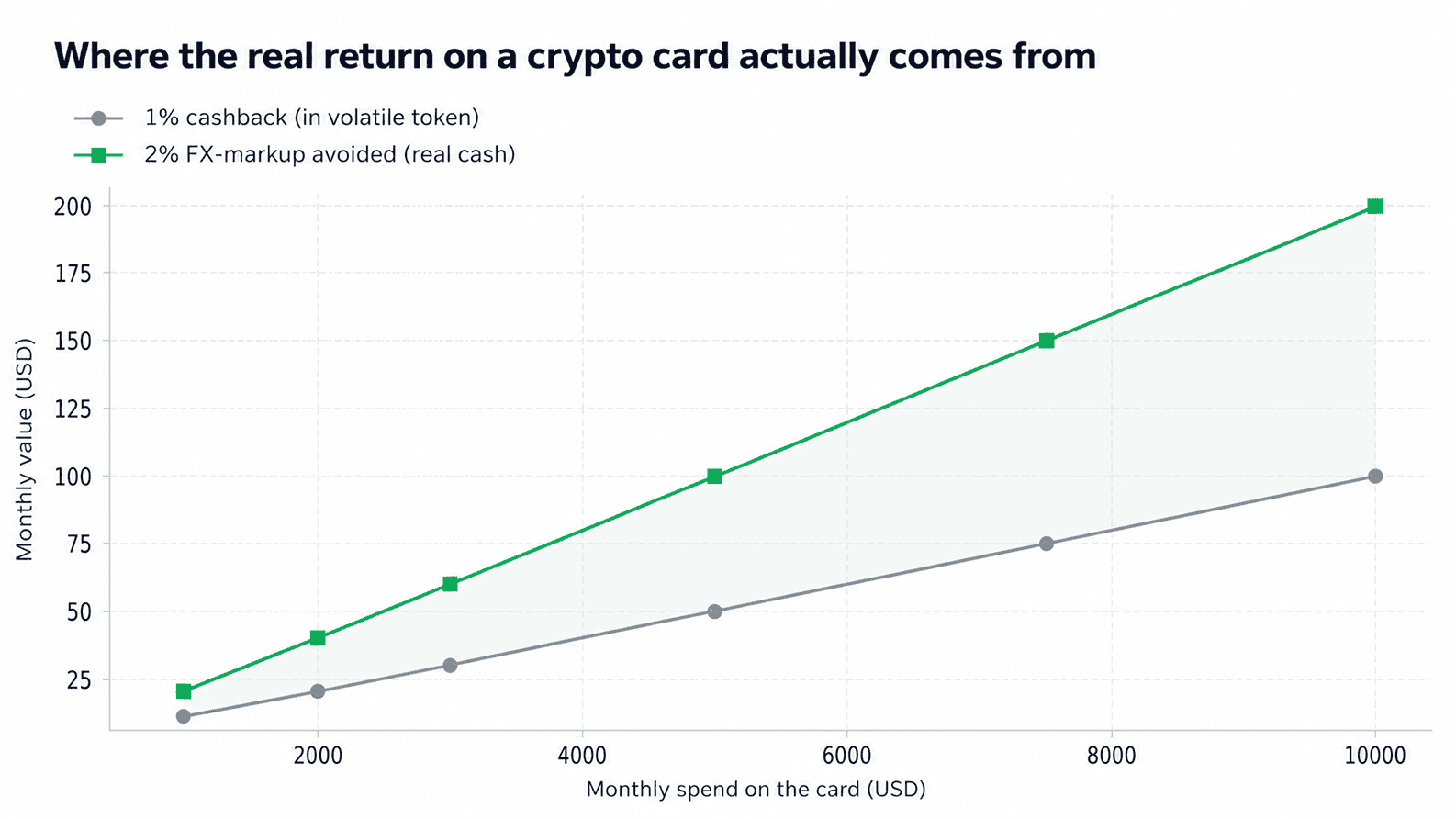

Story 4: The Cashback Mirage

Most card providers advertise rewards. Some offer small cashback. Others promise higher rewards if the user holds or stakes a platform token. This is where freelancers should slow down.

The useful question is not “how much cashback can I earn?” The useful question is whether the card reduces payment friction without adding a bigger risk somewhere else.

If a card saves 2% on cross-border conversion but pays 1% cashback in a token the freelancer does not want, the real value is the FX saving, not the reward. If the reward depends on holding a volatile token, the freelancer is no longer just optimizing payments. They are taking an investment position.

A cleaner model is EUR-based cashback rather than token-based cashback. Some providers pay rewards in euros, not platform tokens. For example, an EMI-licensed payment account with an

integrated crypto service can let a freelancer receive crypto, manually convert it into EUR, and then use a separate EUR balance for everyday spending through a

payment card. In that model, the cashback is earned in fiat, with no token volatility and no staking requirement.

For most users, a crypto card for freelancers is attractive because it may reduce delays, simplify international spending, or help convert crypto income into local currency. Cashback should be treated as a bonus, not the reason to use the product.

Illustrative comparison of 1% token cashback against 2% avoided FX markup, plotted across realistic monthly spend levels.

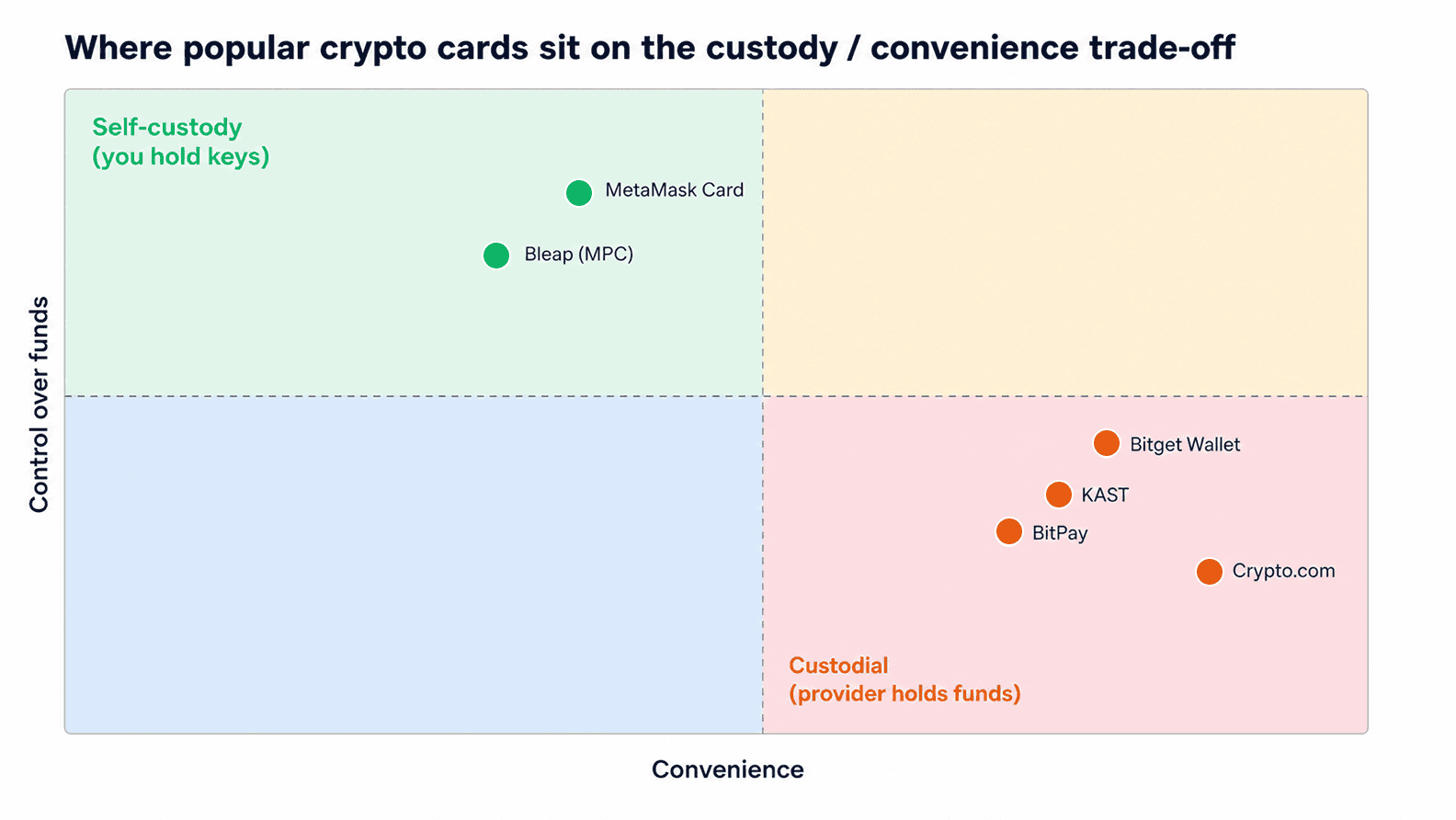

Story 5: Custody Risk

Most card-linked wallets are custodial. That means the provider, not the freelancer, controls the assets until they are spent or withdrawn. If the provider freezes the account for KYC review, sanctions screening, suspicious activity, or internal risk checks, the user may have to wait.

This is the part that marketing rarely emphasizes. A card can be convenient, but convenience often comes from giving a third party control over the funds. A non-custodial setup may reduce that risk, but it usually requires more technical comfort and is not available everywhere.

A practical rule is simple: do not keep all working capital on a card-linked wallet. Load what you expect to spend. Keep emergency funds somewhere else. Export transaction histories regularly.

Indicative positioning of popular crypto cards on the custody/convenience trade-off. Provider features change frequently — check current documentation before relying on this map.

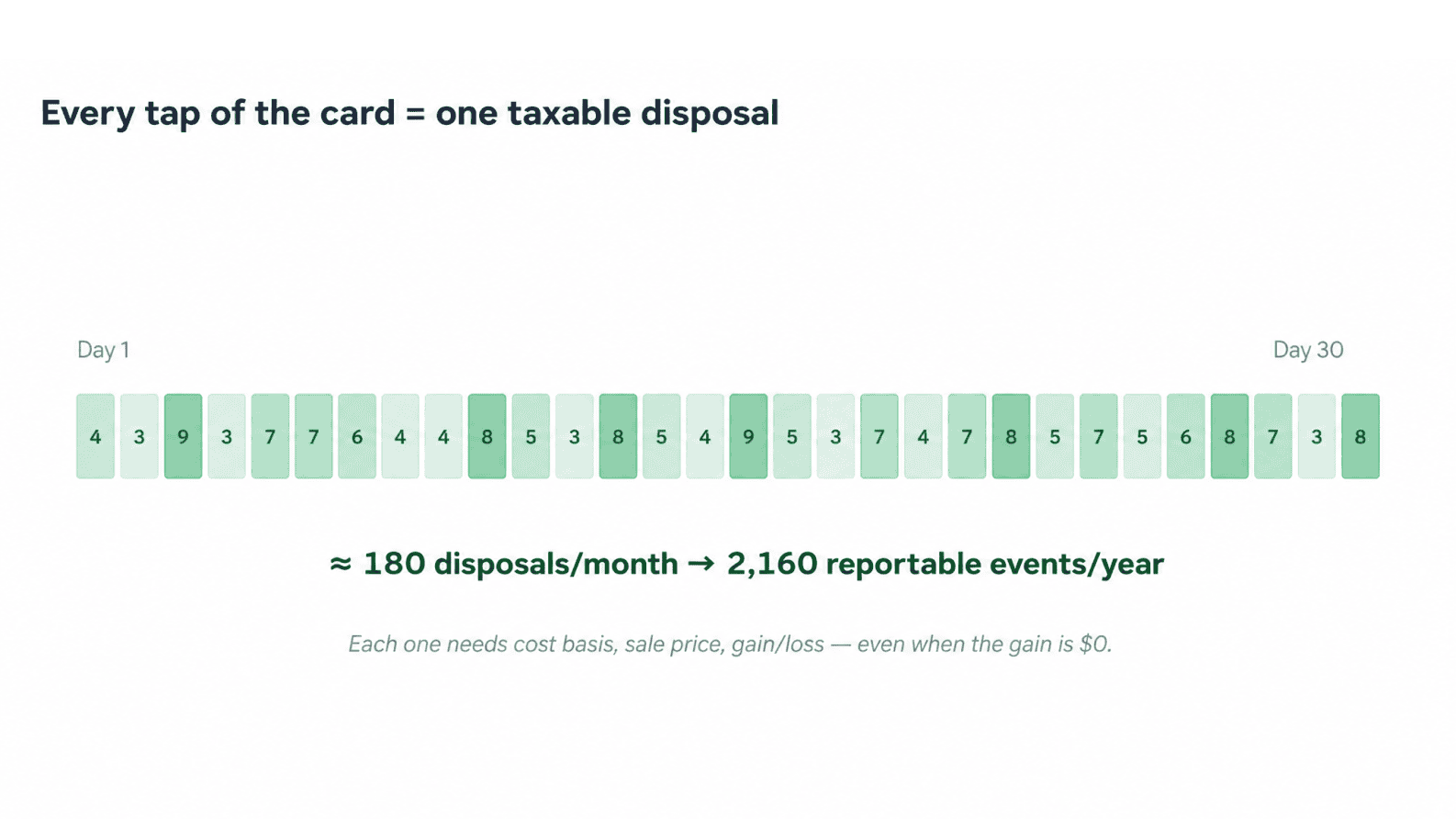

Story 6: The Tax-Event Trap

In many jurisdictions, converting crypto into fiat may be treated as a disposal or taxable event. When you tap a crypto card, you may be selling a small amount of stablecoin for the equivalent value in local currency. The gain may be close to zero if the stablecoin tracks its reference currency, but the crypto tax reporting obligation may still exist.

Tax treatment varies by country. In the United States, the IRS says digital-asset income can be taxable and taxpayers may have reporting obligations for digital-asset transactions. In the UK, HMRC treats using tokens to pay for goods or services as a disposal, which may require the user to calculate a gain or loss for Capital Gains Tax purposes. At EU level, DAC8 introduces tax-transparency rules for crypto-assets, including automatic exchange of information between EU tax authorities. For European freelancers, this means crypto-card spending should be treated not just as a payment convenience, but also as a crypto tax reporting and record-keeping issue.

This is where a two-step crypto-to-EUR model can be cleaner than a card that sells crypto at every transaction. Platforms that let freelancers convert crypto into EUR on their own schedule, and then spend those euros with a standard fiat payment card, may reduce the number of crypto tax events linked to everyday spending. In that structure, the key crypto disposal is usually the conversion into EUR, rather than every individual card tap. For freelancers receiving crypto income, this can make crypto tax reporting easier, although the exact treatment still depends on local tax rules.

This matters for anyone asking, can I use crypto income for everyday payments? Practically, yes, in many places. Administratively, it can create a lot of small records. If a freelancer makes 180 card transactions a month, that can become a large reporting file by year-end. Before committing to a crypto to euro card, crypto-enabled payment app, or card-linked wallet, export a sample month and show it to a tax professional.

Why every crypto card tap can create a separate taxable crypto disposal event — even when the realized gain is near zero. Treatment varies by jurisdiction.

Why every card tap can create a separate disposal event — even when the realized gain is near zero. Treatment varies by jurisdiction.

Cost Comparison: $2,000 Invoice

The numbers below are illustrative, drawn from a small sample of freelance invoices and payment corridors I have reviewed. They are not published benchmarks. The World Bank’s remittance database shows that cross-border transfers still carry meaningful average costs globally, with the global average cost of sending remittances reported at 6.36% in its September 2025 data.

| Cost component | Bank transfer (SWIFT) | Stablecoin + card route |

|---|---|---|

| Sender fee | $25–$45 | $0–$5 network fee |

| Correspondent bank fee | $10–$25 | $0 |

| Receiver bank fee | $5–$20 | $0 |

| FX markup | ~ 2.5% (~ $50 on $2k) | ~0.5–1% at point of sale |

| Settlement time | 2–5 business days | ~30 seconds |

| Estimated total cost on $2,000 | $90–$140 | $10–$25 |

Estimated cost breakdown on a $2,000 monthly client invoice. Figures are author's estimates and should not be treated as published benchmarks.

The Catches Nobody Markets

- Before using any crypto card for freelancers or crypto-enabled payment product, freelancers should check the following:

- Custody: Who controls the funds before spending? Is the crypto held by the user, by a wallet provider, or by an integrated crypto service?

- Product structure: Is the card directly linked to a crypto wallet, or are crypto conversion and fiat spending separate? This matters because Blackcat does not work like a typical crypto card directly connected to a wallet. With Blackcat, the user receives crypto through an integrated crypto service in the app, manually converts it into EUR, and then spends from an IBAN payment account using a fiat payment card.

- Tax reporting: Can you export clean transaction records showing crypto receipts, EUR conversions, and card spending?

- Regional availability: Does the product work in your country and your client’s country?

- EUR conversion: If you need a crypto to euro card or crypto-to-EUR payment workflow, check the actual conversion spread and any fees.

- Mobile wallet support: If you need an Apple Pay crypto wallet or Google Pay crypto wallet experience, check whether the fiat payment card supports Apple Pay or Google Pay before signing up.

- Platform rules: Do not bypass marketplace payment rules. If your freelance work is through a platform, follow its payment terms.

- Backup method: Keep another payment method ready in case the card, wallet, payment account, or crypto service is frozen, delayed, or declined.

FAQ

Can freelancers use a crypto card for everyday spending?

Yes, in countries where the product is available and lawful. The better question is not only can freelancers use a crypto card, but whether the card is suitable for the freelancer’s income, tax position, and location. It can work for subscriptions, travel, groceries, and online purchases, but users should check fees, custody, tax reporting, and platform-payment rules first.

How does a crypto wallet with a payment card work?

Put simply, how do crypto cards work for freelancers? The freelancer receives or holds crypto, usually stablecoins, in a wallet. The card provider converts part of that balance into fiat when the user pays. The merchant receives normal currency. This is why the product is better understood as a wallet-to-fiat bridge than direct crypto spending.

Can I receive crypto and spend euros with a card?

Yes, where supported. The question can I receive crypto and spend euros usually refers to receiving stablecoins and using a card that converts the balance into EUR at payment. This can be useful for freelancers with European expenses, but they should check conversion spreads, card availability, tax treatment, and whether their country permits this use.

Why are freelancers moving away from traditional transfers?

Freelancers are moving because traditional transfers can be slow, expensive, and unpredictable. International payments may involve sender fees, intermediary fees, receiving-bank fees, FX markups, and delays. A card-linked stablecoin route may reduce some of that friction, especially for freelancers in countries where banking access or currency conversion is difficult.

What should freelancers check before using a crypto card?

Freelancers should check custody, fees, tax records, supported countries, EUR conversion rates, card limits, wallet security, and customer support. They should also confirm whether the product is custodial or non-custodial. Most importantly, if the work is through a platform, they must follow that platform’s payment rules and avoid off-platform payments where prohibited.

Can crypto wallets help with cross-border freelance payments?

Yes, crypto wallets can help with cross-border freelance payments in some corridors, especially where bank transfers are expensive or slow. But they are not a universal solution. Local law, tax treatment, client preference, stablecoin access, and card availability all matter. A crypto wallet may solve one payment problem while creating a reporting or custody problem.

Is a crypto card the same as paying directly in crypto?

No. A crypto card is usually not the same as paying directly in crypto. In most cases, the provider converts crypto into fiat before or during the transaction. The merchant receives local currency, not stablecoins. That is why card spending may still create conversion records, fees, and tax reporting obligations.

How can freelancers convert crypto income into EUR?

Freelancers can convert crypto income into EUR through a supported wallet, exchange, or crypto-enabled payment app. A cleaner model is the receive → convert in-app → spend from EUR IBAN structure: the freelancer receives crypto through an

integrated crypto service, manually converts it into EUR when ready, and then spends from a EUR IBAN payment account using a fiat payment card. This can be easier to manage than a card that sells crypto at every transaction, but freelancers should still compare fees, conversion spreads, tax treatment, and transaction-history quality before relying on one provider.

Is Blackcat a crypto card?

Blackcat should not be understood as a typical crypto card directly linked to a crypto wallet. Its model is different. The user can receive crypto through an integrated crypto service in the app, manually convert it into EUR, and then spend EUR from an IBAN payment account using a fiat payment card. The crypto and card features are separate, which may give freelancers more control over conversion and spending.

Summary

A crypto card is not a financial revolution. It is a workaround — sometimes a clever one — for freelancers dealing with slow, expensive, and uneven international payments. The freelancers I have watched make the switch are not usually trying to make a statement about crypto. They are trying to keep more of what they earn, receive money faster, and spend across borders with less friction.

The strongest case is practical: cross-border clients, repeated FX losses, delayed bank wires, and everyday expenses in another currency. The weakest case is marketing: cashback, token rewards, and vague claims about “spending crypto.” Treat the card as what it is: a payment bridge between a crypto balance and ordinary fiat spending.

For some freelancers, it will make sense. For others, a traditional bank or regulated payment account will still be simpler. The answer depends on income source, country, tax position, risk tolerance, and whether the freelancer can keep proper records.

For freelancers who earn in crypto but want clean EUR spending, a two-step crypto-to-EUR setup offers practical benefits: receive crypto, convert into EUR when ready, and spend in euros with a payment card. Platforms like Blackcat combine an integrated crypto service with a European payment account and card, keeping crypto and fiat in one app without merging them into one payment flow.

Disclaimer

This article is for informational purposes only. Readers should consult a qualified financial adviser, tax professional, or lawyer before making decisions about cross-border payments, stablecoin use, or crypto-linked card products.

Share this article