How to Receive Money from Abroad Without Losing It to Fees

By

Emma Carter

27.05.2026

11 min

If you freelance from Europe for clients in the US, receive a salary from a UK employer, or get platform payouts in dollars from YouTube or Patreon — you have probably noticed the same thing: the amount that lands in your account is smaller than what was sent. Sometimes noticeably smaller.

That gap is not a glitch. It is the combined result of transfer fees, exchange rate markups, and intermediary deductions that pile up between the sender’s outbox and your account balance. For freelancers, expats, and content creators living in Europe and receiving cross-border income, these costs are a recurring tax on every payment — and most people never see a clear breakdown of where the money actually goes.

This article is for you if you live in Europe (EU, EEA, or UK) and regularly receive payments from abroad — whether from the US, UK, UAE, Switzerland, or other EU countries. We will break down exactly how international transfer fees work, explain why the route your payment takes matters more than the headline fee, and share practical strategies that real freelancers and expats are using in 2026 to keep significantly more of every incoming payment.

Where Your Money Disappears: The Four Fee Layers

International transfers are not a single transaction — they are a chain, and every link can extract a fee. The problem is that most of these fees are invisible until the money arrives. Here are the four layers that quietly reduce what you receive.

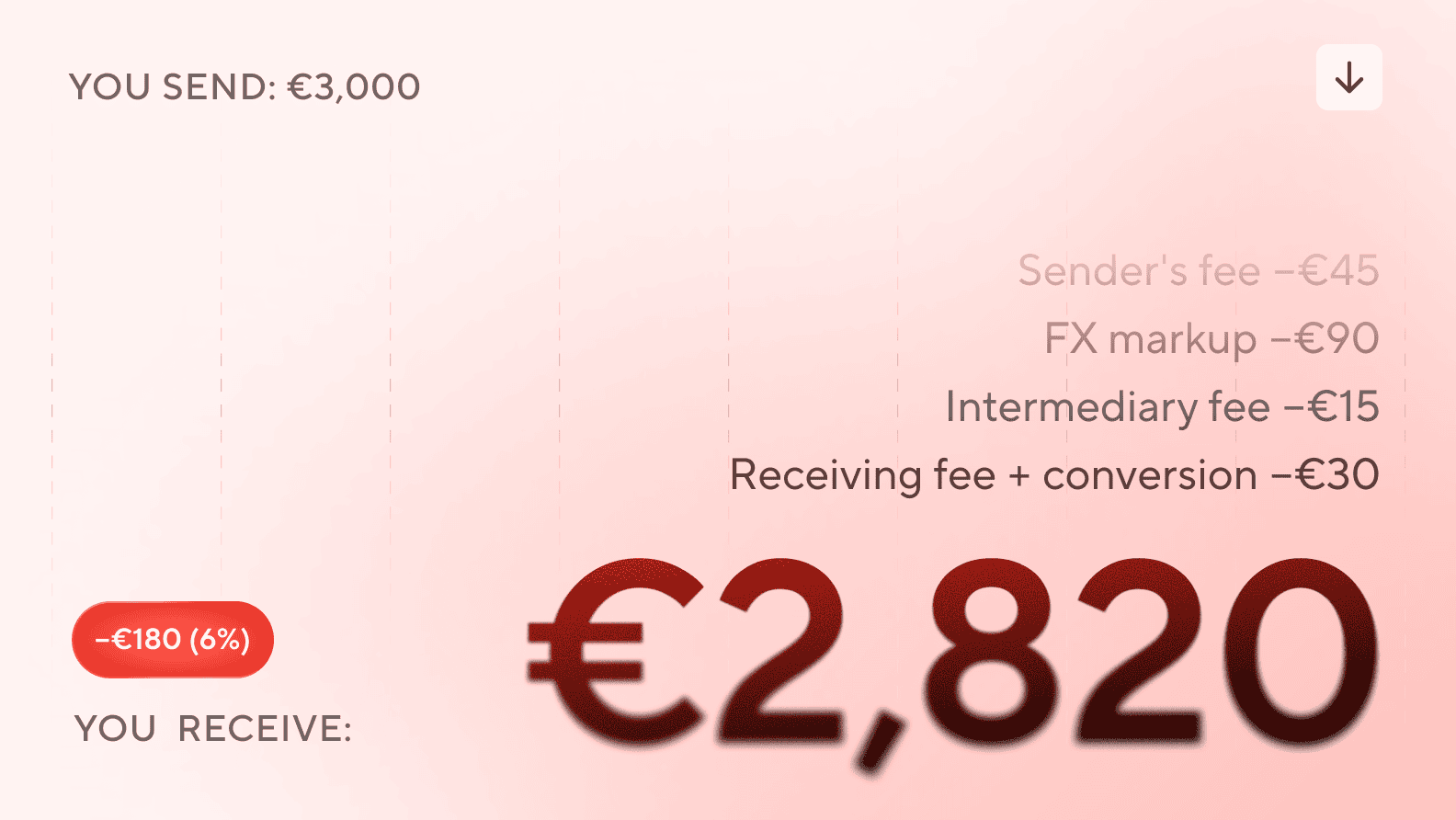

Layer 1: The sender’s outgoing fee

This is the only fee most people are aware of, and it is paid by the sender — not you. But it still affects you: on smaller payments, the sender may reduce what they send to offset the fee, or the fee may simply shrink the total amount in transit. A traditional SWIFT payment from a US institution typically costs $35–$50. UK high-street providers charge £20–£35 for an outgoing international wire. These fees are fixed regardless of the amount, which means they disproportionately punish smaller transfers. On a $500 payment, a $45 fee alone is 9%.

Layer 2: The exchange rate markup

This is where the biggest hidden cost lives. When a provider says “no transfer fees,” they almost always compensate by widening the spread between the mid-market rate (the real rate you see on Google or Reuters) and the rate they actually give you. Traditional providers commonly apply a markup of 2–5%. On a $5,000 payment from a US client, a 3% markup silently removes $150 before you even see the money. Specialist fintech providers typically charge under 1%, and some guarantee the mid-market rate with a small transparent fee on top.

Layer 3: Intermediary (correspondent) deductions

When a SWIFT payment travels from one country to another, it often passes through one or more correspondent institutions that facilitate the transfer. Each intermediary can deduct a handling fee — typically €5–€20 per hop — directly from the transfer amount. You only discover these deductions when the final amount hits your account and it is less than expected. For a payment from the US to Europe, one or two intermediary hops are common.

Layer 4: The receiving fee and forced conversion

Many providers charge simply for receiving an international payment. In the UK, incoming wire fees range from £2 to £7.50. On top of that, if the incoming currency does not match your account currency, your provider may automatically convert it at their own rate — not the market rate. This forced conversion can add another 1–3% in hidden costs, and you have no control over the timing or the rate.

What does this add up to? On a typical $3,000 freelance payment from the US via a traditional SWIFT route, total costs of $150–$300 are common — that is 5–10% of the transfer. Even on a UK-to-EU corridor, where the distance is shorter but the FX markup still applies, freelancers regularly lose 3–6% per payment through traditional channels. Over a year of monthly payments, that is €1,000–€3,000 in lost income.

Note: These ranges are based on published industry data from WorldFirst, MyCurrencyTransfer, Bankrate, and NerdWallet (2026). The exact cost depends on the specific providers, currency pair, and transfer amount. Intra-eurozone SEPA transfers are dramatically cheaper — more on that below.

SWIFT vs. SEPA: Why the Route Matters More Than the Fee

If you live in Europe and receive payments from within the SEPA zone, choosing the right payment route is the single biggest thing you can do to cut costs. The difference between SWIFT and SEPA is not incremental — it is fundamental.

SWIFT is a global messaging network connecting over 11,000 institutions in 200+ countries. It handles payments in any currency, but the actual money hops between correspondent institutions — each potentially taking a cut. It is slow (1–5 business days), expensive, and unpredictable in terms of what the recipient actually receives.

SEPA (Single Euro Payments Area) is a euro-specific payment rail covering 41 European countries including all EU member states plus Iceland, Liechtenstein, Norway, Switzerland, and the UK. It was designed to make cross-border EUR transfers within Europe as cheap and simple as domestic ones. Under EU regulation, the full amount must arrive — no intermediary deductions. And since the EU’s Instant Payments Regulation rolled out through 2025, most providers in the eurozone now support SEPA Instant — meaning transfers can arrive in under 10 seconds, around the clock, including weekends. (Some smaller institutions are still completing the rollout, but coverage is broad and growing.)

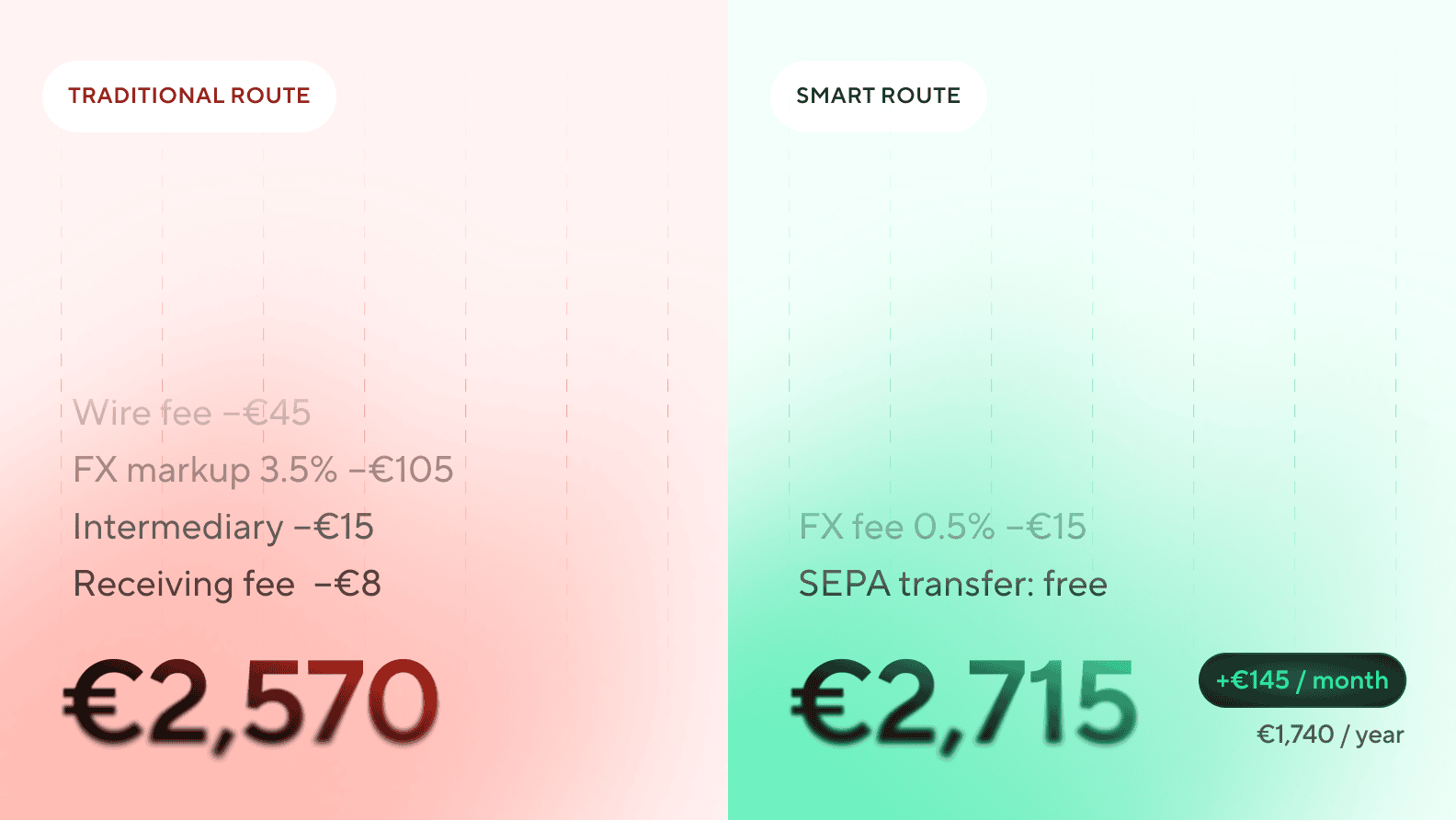

SWIFT vs. SEPA at a glance

| SWIFT | SEPA | |

|---|---|---|

| Currencies | Any | EUR only |

| Coverage | 200+ countries | 41 European countries |

| Speed | 1–5 business days | 0–3 business days / Instant (<10 sec) |

| Intermediary fees | Yes (€5–€20 per hop) | None |

| Amount deductions en route | Common | Prohibited by regulation |

| Typical total cost (receiver) | 3–10% on non-EUR corridors | €0–€2 |

The practical takeaway: if your client or platform is within a SEPA country and can send EUR, there is almost never a reason to receive via SWIFT. A SEPA transfer in euros from the UK to your EUR IBAN in Germany, Malta, or France will typically arrive within 1–3 business days (or seconds via SEPA Instant), cost less, and the full amount arrives intact.

💡 Worth noting: The UK left the EU but remains a SEPA participant. However, not all UK providers still support SEPA — some have dropped SEPA connectivity since Brexit. If your client's provider does support it, they can send EUR via SEPA to any European IBAN. It is worth confirming with the sender first. Many freelancers do not realise this option exists and accept GBP SWIFT wires by default, paying unnecessary fees on every transfer.

Five Strategies That Actually Reduce What You Lose

Based on conversations with dozens of freelancers and expats across Europe, these are the patterns that consistently make the biggest difference.

1 . If your client is in Europe: make sure they send via SEPA, not SWIFT

This is the most common and most fixable problem. You have a EUR IBAN. Your client is in Europe or the UK. But the money still arrives via SWIFT — with all the correspondent deductions and delays — because nobody told the sender to use SEPA. It happens constantly: the client enters your IBAN into an international wire form instead of a SEPA transfer form, and your simple euro payment takes an expensive detour.

The fix takes two minutes. Put your IBAN and BIC on every invoice with an explicit note: “Please send as a

SEPA transfer in EUR (not international wire).” A freelance translator in Vienna shared with us that she had been losing €15–€20 per payment from her three EU-based clients for over a year. All three were sending SWIFT wires to her IBAN. One email to each client fixed it permanently — saving her roughly €50–60 per month.

2 . If your client is outside Europe: ask if they can pay in EUR

This is separate from the first point because it applies to clients outside Europe — particularly in the US. Some US companies — especially larger ones or those already set up for international payments — can send payments in EUR if you ask. When they do, the payment can travel via SEPA-compatible routes or at least avoid the worst USD-to-EUR conversion markups at your end. Not every client will accommodate this, but it costs nothing to ask, and the savings can be substantial.

A UX designer based in Lisbon told us her main US client had been paying in USD via SWIFT for two years. When she asked if they could switch to EUR, the client’s finance team said yes immediately — it cost them roughly the same on their side. On her side, the total fees dropped from around €90 per payment to under €10. On monthly $4,000 invoices, that change alone saved her over €900 per year.

3 . Stop letting your provider auto-convert your incoming payments

If you receive a payment in USD or GBP and your account is in EUR, many providers will automatically convert it the moment it arrives — at their exchange rate, not the market rate. That auto-conversion can cost 1.5–3% on top of everything else.

If your provider allows you to hold multiple currencies or use separate wallets, receive the funds in the original currency and convert manually when the rate is favourable. This gives you control over both the timing and the cost of conversion. Even waiting a day or two for a better rate can make a meaningful difference on a €3,000–€5,000 payment. Not all providers offer multi-currency holding — if yours does not, it may be worth switching to one that does, especially if you receive non-EUR income regularly.

4 . Consolidate into fewer, larger transfers

Every SWIFT transfer carries fixed costs regardless of the amount. A $500 payment and a $5,000 payment often incur the same $45 wire fee — but that fee is 9% of the smaller amount and less than 1% of the larger one. If you receive many small payments (weekly platform payouts, per-project invoices), negotiate monthly or bi-weekly cycles instead. One e-commerce seller in Warsaw told us he was receiving bi-weekly payouts of $500–$800 via SWIFT, losing 5–7% each time. When he switched to monthly $2,000 payouts in EUR, his total transfer costs dropped to under 1%.

5 . Compare total landed cost, not just the headline fee

A provider that advertises “zero fees” but applies a 3.5% exchange rate markup will cost you far more than one that charges €5 but uses the mid-market rate. The only number that matters is the total amount that actually arrives in your account. Before accepting a new payment route, calculate: amount sent minus all fees, minus FX markup, minus intermediary deductions, minus receiving charges. That final number is what you compare.

A realistic note: not every client or platform will accommodate these changes. Some have fixed payroll systems or limited payout options. But in our experience, more will than you might expect — especially if you frame it as a simple preference rather than a demand. Even switching one or two regular payers to a better route can save you hundreds per year.

When Crypto-to-Euro Conversion Actually Makes Sense

For some freelancers and creators, cryptocurrency has become a practical payment rail — not because they are crypto enthusiasts, but because it solves a specific problem: receiving money from outside Europe quickly and without intermediary deductions.

The scenario typically looks like this: a US-based client or platform sends you USDC (a dollar-pegged stablecoin). You receive it in a wallet and convert it to EUR. The converted euros arrive in your payment account, ready to spend or transfer via SEPA. The total cost of this flow — including the conversion spread — can be lower than a traditional SWIFT wire, especially on corridors where SWIFT fees and FX markups are high (US → EU, UAE → EU).

A freelance developer in Tallinn told us he switched to receiving a portion of his US client payments in USDC. On a €3,000-equivalent payment, his total cost dropped from roughly €130 via SWIFT (wire fee + 3% FX markup + intermediary) to about €30–45 through stablecoin conversion. That is a significant saving, but it comes with caveats: conversion spreads vary between platforms, network fees can fluctuate (though they are generally low for stablecoins on modern networks), and there may be tax implications in your jurisdiction.

This approach works best for people who already understand how wallets work and are comfortable with the process. It is not a universal solution, but for specific corridors where traditional transfers are expensive, it is worth considering — especially when using an app that bridges crypto and fiat in one place.

How Blackcat Helps With This

We built Blackcat for exactly the kind of person this article is about: someone living in Europe who needs a reliable, low-cost way to receive money from abroad and manage it in one place.

Blackcat gives you a personal EUR IBAN connected to the SEPA network. When someone sends you a SEPA transfer — from any of the 41 participating countries — the full amount arrives in your account, typically same-day or instantly if the sender supports SEPA Instant. No intermediary deductions and a clear, predictable fee structure.

For income that arrives in crypto (stablecoins, Bitcoin, Ethereum), the Blackcat app includes an integrated crypto service where you can receive digital assets from external wallets, convert them into euros, and hold or transfer the resulting EUR via SEPA — all within the same app. This is particularly useful for freelancers and creators who earn in both fiat and crypto and want to avoid juggling separate platforms.

You can also use separate wallets within the app to organise your money by purpose — for example, separating business income from personal spending, or setting aside funds for taxes. And the Blackcat payment card works as a credit-grade card, meaning it is accepted for hotel bookings, car rentals, and other transactions that typically require a credit card.

Summary

Receiving money from abroad does not have to mean losing 5–10% on every payment through traditional cross-border routes. The costs are real, but they are also avoidable once you understand where they come from and which routes to use.

For payments from within Europe: make sure your payers send EUR via SEPA to your IBAN. This eliminates intermediary fees, guarantees the full amount arrives, and with SEPA Instant, means your money can arrive in seconds. If your payers are currently using SWIFT for euro payments — which happens more often than you would expect — a single conversation can fix it permanently.

For payments from outside Europe (US, UAE, etc.): ask if the sender can pay in EUR to reduce conversion costs on your side. Use a provider with transparent FX pricing rather than letting a traditional institution handle the conversion at their markup. Consider consolidating smaller payments into larger monthly transfers. And for specific corridors where traditional fees are high, crypto-to-euro conversion through stablecoins can be a practical alternative.

The difference between a poorly optimised receiving setup and a well-chosen one can easily be €1,000–€2,000 per year for someone receiving regular cross-border income. That is real money — and it belongs in your account.

FAQ

Is receiving a SEPA transfer free?

In most cases, yes. EU regulations prohibit providers from deducting fees from the transfer amount itself. Many fintech providers charge nothing for incoming

SEPA transfers. Some traditional institutions charge a small fee (typically under €2), but the full amount always arrives.

Can I receive SEPA transfers from the UK?

Yes. The UK remains a SEPA participant after Brexit, but some UK providers have dropped SEPA connectivity. UK-based clients and employers can send EUR via SEPA to any European IBAN. This is one of the most underused facts in cross-border payments for freelancers.

How fast is a SEPA transfer?

A standard SEPA credit transfer can take up to 3 business days, though most arrive within 1 working day. SEPA Instant, which the EU has required most providers to support since 2025, settles in under 10 seconds, 24/7, including weekends and holidays.

What is the cheapest way to receive money from the US in Europe?

It depends on the amount and frequency. For regular payments, asking the sender to pay in EUR (which can then route via SEPA) is often the cheapest option. For USD payments, using a provider with transparent FX pricing and no intermediary fees can reduce total costs by 70–90% compared to a traditional SWIFT wire. For specific use cases, stablecoin transfers (e.g., USDC) offer another low-cost alternative.

How do I avoid hidden exchange rate markups?

Compare the rate your provider offers against the mid-market rate on Google or a site like XE.com. The difference is the markup. Providers that explicitly show you the mid-market rate and charge a separate transparent fee are almost always cheaper than those that say “no fees” but hide the cost in the exchange rate.

Share this article