How to Separate Your Personal and Freelance Money — And Why It Matters for Taxes

By

Emma Carter

28.04.2026

9 min

I spent the first year of my freelance career running everything through one payment account. Client payments, groceries, software subscriptions, rent — all flowing into and out of the same place. It felt simple until January arrived and I sat down to file taxes. Three weeks later, I was still sorting through transactions trying to figure out which €47.90 charge was a client lunch and which was Tuesday dinner with friends. I ended up missing roughly €1,200 in legitimate deductions that year, purely because I could not reconstruct what was business and what was personal.

This article covers how to separate personal and freelance money in a way that actually works day-to-day, why the separation matters far beyond just tidiness, what specifically changes when tax season arrives, and how different European jurisdictions treat the question. It draws on conversations with freelancers, accountants, and compliance professionals across Europe, plus the hard lessons of doing it wrong myself.

The Real Cost of the Single-Account Approach

Most freelancers start the same way. You get your first client, they ask for payment details, and you give them your personal IBAN. It works. Money arrives. You spend it. The problem builds slowly and becomes visible only when you need to account for what happened.

A tax advisor I spoke with in Berlin told me that the vast majority of freelancers who come to her for help with their first Einkommensteuererklärung have never separated their finances. “They show up with twelve months of bank statements and a vague sense of dread,” she said. “We spend the first three sessions just categorising transactions that should have been obvious from day one.”

The financial cost is not abstract. When business and personal transactions are mixed, three things happen reliably:

You miss deductions. A €15 monthly software subscription is easy to spot in your statement. A €3.50 cloud storage fee buried between a supermarket charge and a streaming subscription? That one slips through. Across a year, these missed small deductions add up to hundreds of euros — in my own first year of mixed bookkeeping I reconstructed roughly €1,200 in legitimate expenses I had never claimed.

You overpay on estimates. When you cannot quickly calculate your actual business profit, you tend to overestimate quarterly tax payments to avoid penalties. That money sits with the tax authority interest-free until you file your annual return and get it back — months later. For a freelancer earning €50,000, overpaying by even 10% means €1,000–2,000 locked away unnecessarily.

You create audit exposure. Tax authorities across Europe have become significantly more sophisticated in flagging self-employed returns that show patterns consistent with commingled finances. In Germany, the

Finanzamt can and does request full account statements during audits. If every transaction is mixed, you are not just defending individual deductions — you are defending the credibility of your entire return.

What Tax Authorities Actually Look For

There is a persistent myth among freelancers that separating personal and business finances is optional — a nice-to-have rather than a practical necessity. Legally, most European jurisdictions do not require a separate account for sole traders. But practically, operating without one is like driving without a dashboard: technically possible, significantly riskier.

Here is what different jurisdictions expect:

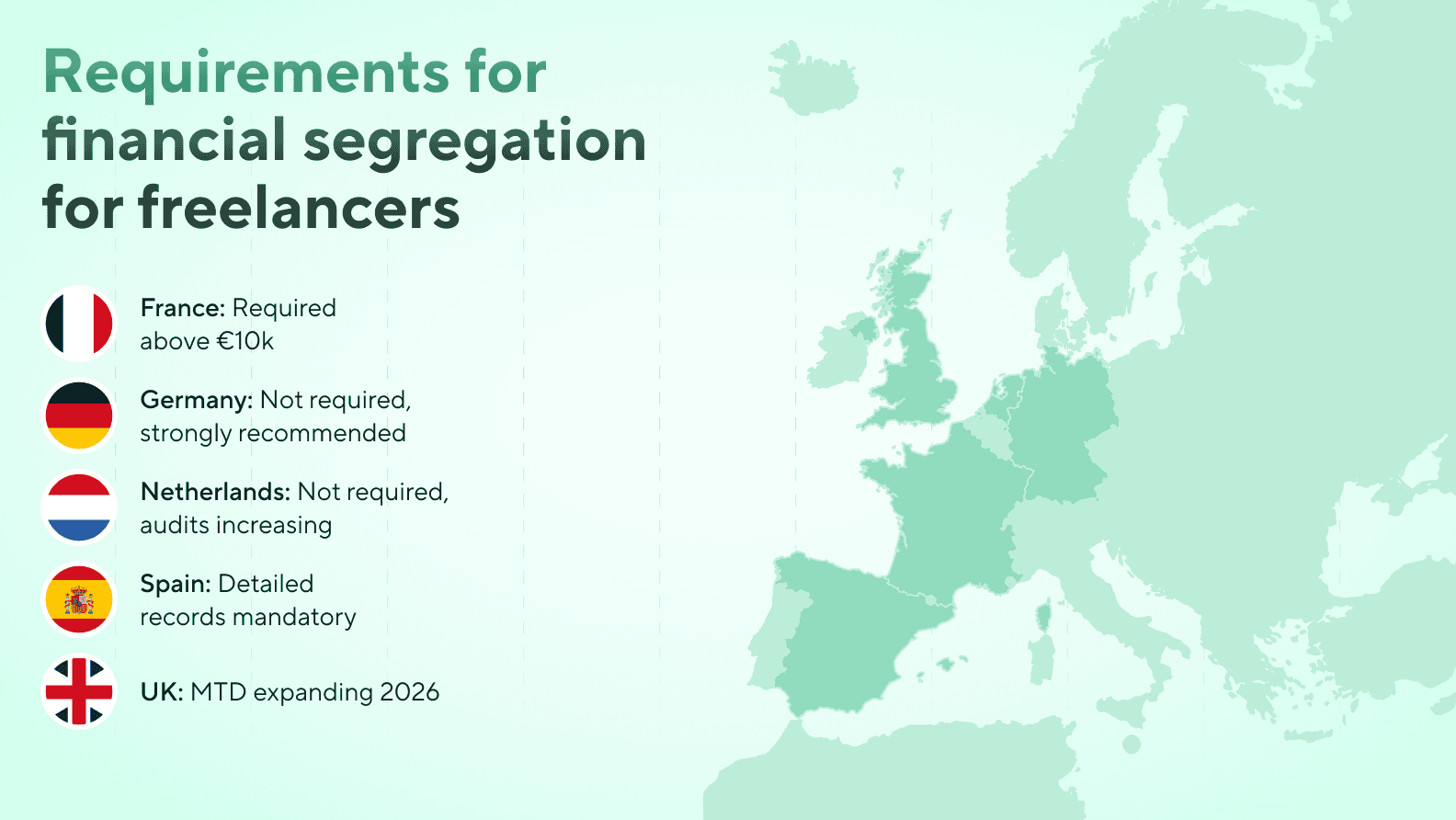

| Country | Legal requirement | Practical reality |

|---|---|---|

| Germany | No legal obligation for Freiberufler to hold a separate business account | The Finanzamt expects clear documentation. Mixed accounts make EÜR preparation significantly harder and raise audit flags |

| France | Micro-entrepreneurs earning above €10,000/year must have a dedicated account since 2019 | Even below the threshold, accountants universally recommend separation for Impôt sur le Revenu clarity |

| UK | No legal requirement for sole traders, but HMRC Self Assessment demands detailed income/expense records | Making Tax Digital (MTD) expansion in 2026 increases digital record-keeping requirements for self-employed with income over £50,000 |

| Netherlands | No separate account required for ZZP’ers | The Belastingdienst cross-references bank data during audits. Clean records are your best defence |

| Spain | Autónomos must keep detailed income and expense records | Hacienda audits have increased since 2023. A dedicated account simplifies the income and expense bookkeeping |

The pattern is consistent across Europe: even where separation is not legally mandated, the practical consequences of not doing it range from inconvenient to expensive.

A freelance translator based in Amsterdam shared her experience: “I got a letter from the Belastingdienst asking me to explain seven specific transactions from 2023. All of them were legitimate business expenses — translation software, a conference ticket, reference books. But because they were mixed in with personal spending on the same account, I had to write individual explanations for each one. It took two full working days. A separate account would have made the whole thing a non-issue.”

The Five-Account Structure That Changed How I Work

After the first-year disaster, I tried the obvious fix: one personal account, one business account. It helped, but it was not enough. The problem was cash flow timing. Client payments are irregular. Tax obligations are not. I would receive a large payment, feel flush, spend some of it, and then scramble when quarterly taxes were due.

The system that actually works — and that several accountants I have spoken with recommend — uses purpose-specific accounts or wallets to create built-in financial discipline:

| Account / wallet | Purpose | Rule | Why it matters |

|---|---|---|---|

| Business incoming | All client payments land here | Nothing personal touches this account. This is the IBAN on your invoices | Creates a clean audit trail from invoice to deposit |

| Tax reserve | Income tax + social contributions | Transfer 25–35% of every incoming payment immediately | Quarterly payments are covered without stress. No surprises at year-end |

| VAT reserve | VAT collected from clients | If VAT-registered, set aside the VAT portion of each invoice | VAT money is never “yours” — treating it separately prevents spending it accidentally |

| Business expenses | Software, equipment, travel, professional development | Fund monthly from business incoming. Pay all business costs from here | Every transaction on this account is deductible by default. Simplifies bookkeeping dramatically |

| Personal | Salary to yourself | Transfer a fixed amount monthly — your “salary” | Forces you to budget as if you were employed. Stops the feast-famine cycle |

This structure looks over-engineered on paper. In practice, it takes about fifteen minutes to set up if your financial services provider supports multiple wallets or sub-accounts, and it saves hours every month in bookkeeping and years of stress at tax time.

Products with

business finance tools that offer multiple wallets within a single app make this particularly straightforward — you can create purpose-specific wallets for tax reserves, business expenses, and personal spending without opening accounts at five different institutions. The key is that each wallet functions as a clear container with a single purpose.

A UX designer I know in Lisbon runs a version of this system and describes the shift: “Before, I was always guessing. Can I afford this conference? Do I have enough for taxes? Now I look at the tax wallet and know immediately. The business expense wallet tells me my runway. It removed the financial anxiety that was actually affecting my work.”

There is a secondary benefit to this structure that most freelancers overlook. The money you set aside for taxes sits in your reserve wallet for weeks or months before it actually goes to the tax authority. For a freelancer earning €50,000 a year and setting aside 30%, that is €15,000 moving through the tax wallet annually — with a rolling balance that often stays in the €3,000–€7,000 range between quarterly payments. In a traditional setup, this money sits idle.

Blackcat gives you access to a 4% p.a. reward* on your EUR balance, paid out monthly in euros, with no need to lock your money in a separate savings account. In practice, this means the discipline of separating your tax money also generates a small return on money you were going to set aside anyway. On a €5,000 rolling tax reserve, that works out to roughly €200 per year — enough to cover an accounting software subscription, or a decent chunk of your year-end tax advisor fee.

VAT, Social Contributions, and the Complications Nobody Warns You About

Separating personal and freelance money sounds simple until VAT enters the picture. If you are VAT-registered — and in many European countries, you will be once your turnover crosses a relatively low threshold — the money your clients pay includes a portion that was never yours to begin with. It belongs to the tax authority.

The thresholds vary significantly across the EU. Germany’s

Kleinunternehmerregelung exempts freelancers with turnover under €25,000 (previous year) and a €100,000 current-year cap as of 2025. France has different thresholds depending on service type. The UK requires VAT registration once taxable turnover exceeds £90,000. And since January 2025, the EU introduced a

new cross-border SME scheme with a €100,000 threshold for exempt selling across member states — relevant if you have clients in multiple EU countries.

The mistake I see most often: freelancers who hit the threshold, register for VAT, and continue operating from a single account. They issue invoices with VAT included, receive the full amount, and mentally count it all as income. When the quarterly VAT return arrives, the money has been spent. This is not a theoretical risk. An accountant in Dublin told me it is the single most common cash-flow crisis she deals with among self-employed clients.

Social contributions add another layer. In Germany, while Freiberufler are exempt from trade tax, they still face health insurance, pension considerations, and potentially the Künstlersozialkasse if they work in creative fields. In France, micro-entrepreneurs pay cotisations sociales that can amount to 22–26% of turnover depending on the activity type, collected monthly or quarterly by URSSAF. In Spain, the autónomo flat rate for new freelancers has been reformed, but contributions still need to be budgeted separately from income tax.

The five-account structure handles all of this, but only if you calibrate the percentages correctly for your jurisdiction. A German Freiberufler earning €60,000 might set aside 25–30% for income tax, plus health insurance premiums separately. A French micro-entrepreneur under the regime might need to budget 22–26% for social contributions paid to URSSAF, plus income tax on top. Getting the split wrong in either direction costs you money — either through penalties or through unnecessary cash sitting idle.

When Crypto and Multi-Currency Freelancing Add Another Layer

An increasing number of European freelancers now receive some portion of their income in cryptocurrency. A developer in Estonia might agree with a US client to be paid in USDC instead of a traditional wire transfer. A content strategist in Berlin might have most clients paying in EUR via SEPA, but one paying in Bitcoin.

This creates two separate tax events that many freelancers confuse. The first is straightforward: when you receive crypto as payment for services, the full market value at the moment of receipt is taxable income — just like receiving euros. You owe income tax on that amount regardless of what happens to the price afterwards.

The second event occurs when you convert that crypto into euros. If the price has changed between receipt and conversion, the difference is a separate taxable gain or loss. In Germany, this falls under

§23 EStG — private disposal transactions. If you hold the crypto for more than one year before selling, the gain is tax-free. But most freelancers convert within days or weeks to cover rent and running costs, which means the gain is fully taxable.

The practical problem is not that fiat and crypto land in the same account — they cannot, because they move on different rails. Crypto arrives in a wallet, euros arrive in your IBAN. The problem is reconciliation: matching the EUR value at the moment you received each crypto payment, tracking the holding period, calculating the gain or loss at conversion, and tying it all back to specific invoices. Do this across two or three platforms with weekly transactions, and year-end bookkeeping becomes genuinely painful.

This is where a single interface that handles both

SEPA transfers and an integrated crypto service matters. Not because it solves the tax complexity — you still need to track each event — but because it reduces the number of platforms you need to reconcile from three or four to one. Every platform you eliminate is a category of missing data you will not have to chase in January.

What 2026 Changed (And What Is Coming Next)

Several regulatory shifts in 2025 and 2026 have made financial separation more important than it was even two years ago:

Making Tax Digital in the UK is expanding. From April 2026, self-employed individuals and landlords with income over £50,000 must use

MTD-compatible software for income tax. This means quarterly digital updates to

HMRC — which is dramatically easier if your business transactions are already cleanly separated and categorised.

The EU’s VAT in the Digital Age (ViDA) package is

rolling out in phases through 2030. Cross-referencing between tax authorities, payment processors, and platforms is becoming automated. Discrepancies between reported income and account activity will be flagged systematically, not randomly. Freelancers with clean financial separation are less likely to trigger false positives.

The EU cross-border SME VAT scheme, live since January 2025, introduces the €100,000 threshold for VAT-exempt selling across member states. For freelancers working with clients in multiple EU countries, tracking whether you are approaching this threshold requires clear visibility into business revenue — which means it needs to be separated from personal spending.

Platform reporting requirements continue to expand. The EU’s

DAC7 directive requires digital platforms to report seller income to tax authorities. If you receive income through platforms alongside direct client payments, and everything lands in a single account, reconciling platform-reported income with your own records becomes unnecessarily complicated.

The direction is clear: European tax enforcement is becoming more digital, more automated, and more cross-border. The freelancers who will navigate this smoothly are the ones who already have their financial house in order. The ones who will struggle are those still running everything through a single account and hoping nobody notices.

FAQ

How do I separate personal and freelance money?

Open a dedicated account or wallet for business income. Set up separate reserves for taxes and VAT. Pay yourself a regular amount into your personal account. The goal is that every transaction in each account has a single, obvious purpose. This approach to separating personal and business finances does not require complex tools — just discipline and the right account structure.

Do freelancers need a separate business account?

In most European countries, sole traders are not legally required to have a business account for self-employed income. France is an exception for micro-entrepreneurs above €10,000. But practically, not having one costs you time, money, and audit risk. Every accountant and tax advisor I have spoken with recommends it without exception.

Can I use my personal account for freelance income?

You can, in most jurisdictions. You should not. Mixing personal and business finances makes it harder to track expenses, easier to miss deductions, and more difficult to defend your return if questioned. The best way to manage self-employed income and payments is to keep them separate from day one.

Why does separating personal and business finances matter for taxes?

Three reasons: you claim more deductions because business expenses are visible, you avoid overpaying quarterly estimates because profit is clear, and you reduce audit risk because your records are credible. For most freelancers, separation pays for itself in the first tax year.

How does a separate account help track freelance expenses?

When every transaction on an account is business-related, categorisation becomes trivial. Your year-end bookkeeping shifts from archaeology — digging through mixed transactions — to verification — confirming what is already organised. This is the difference between three weeks of stress and an afternoon of routine.

What is the best way to manage self-employed income and payments?

Use the multi-wallet approach: separate containers for incoming revenue, tax reserves, business expenses, and personal spending.

Account solutions for self-employed finances that support multiple wallets let you do this within a single app, simplifying the setup without sacrificing the separation. Pair it with accounting software that can pull transaction data automatically, and you have a system that runs itself.

Summary

Separating personal and freelance money is not an administrative luxury. It is the single highest-return financial decision a freelancer can make, measured in recovered deductions, avoided penalties, reduced stress, and hours of life not spent reconstructing what happened in your account last March.

The structure does not need to be complicated. A dedicated business incoming account, a tax reserve, a VAT reserve if applicable, an expense account, and a personal account for your salary. Set the percentages for your jurisdiction, automate the transfers, and forget about it until tax season — when you will wonder why you ever did it any other way.

European tax enforcement is getting more digital and more automated every year. The freelancers who separate early will barely notice. The ones who wait will notice a lot.

This article is based on my own experience as a freelancer in Europe and conversations with accountants and other self-employed professionals. It is not tax, legal, or financial advice. Tax rules vary by country, change regularly, and depend on your specific situation. For decisions about your own finances and tax obligations, please consult a qualified tax advisor or accountant in your jurisdiction.

*The bonus payment is a part of the loyalty program provided by Baltic Technology Solutions OÜ. Detailed terms and conditions can be found at

BaltictechsolutionsLoyalty Program Terms And Conditions

About the Author

Emma Carter is a Financial Editor at Blackcat. She covers personal finance, digital payments, and financial products across the EU and UK, working closely with product and compliance teams to turn complex financial topics into clear, structured articles for freelancers, expats, and everyday users.

Share this article