Next chapter in Open banking: What businesses, fintechs, and consumers should expect

By

Davor Zilic

14.04.2026

7 min

Introduction: The Open banking future

Open banking future is here, and it’s already truly reshaping how we manage, move, and make sense of money at great pace. Already since the introduction of PSD2 in January 2016, both consumers and businesses have enjoyed greater control over their financial information, directly and indirectly via different new business models enabled by such (first and foremost) regulatory initiative. Today with the EU’s Financial Data Access (FiDA) framework and PSD3, open banking in Europe is evolving into even broader open finance, expanding relatively simple account data sharing primarily used in payments to savings, loans, investments and insurance. Looking ahead, the future of open banking will be even more defined by collaboration, innovation, and the democratization of financial services. In this article, we’ll explore how open banking is transitioning to open finance and what exactly that means for you, what are the key trends driving the change of the financial industry, and what is the future of such financial services.

Open banking financial services are also becoming a more important part of this shift for both businesses and fintechs.

Evolution: From Open banking to Open finance

Open banking is no longer just about sharing payment account data, and now with the next chapter in open banking becoming the broader open finance, data sharing will extend to a much broader range of financial products. The EU’s FiDA framework, for example, creates a consistent structure for sharing data on savings, loans, investments and insurance, enabling more personalized and competitive financial services for all personal financial needs. In the UK as well, the push for open finance already for years is ambitious, and now with the Data Use and Access Bill, new so-called “Smart data schemes” it extends also beyond core banking services.

What does open finance mean for fintechs? It means much better access to financial data provided by the traditional financial institutions, enabling them to build new business model, more innovative products and services for their users. Almost every fintech launched over the last couple of years integrated at least one open banking API, which highlight its importance and role as a core infrastructure for financial innovation.

Secondly, you might be wondering how businesses can benefit from open finance. By leveraging APIs, businesses may automate reconciliation and liquidity management, access real-time financial visibility across different providers, or integrate multi-rail payment systems for optimised and cost-efficient transactions. Example of this can also be found in the UK, where Starling Bank and Monzo already offer quite robust developer marketplaces for businesses, which enables integration of open banking features across stakeholders.

Thirdly, Europe remains a leader in open banking (already dominating the market with

market share of >30% in 2025) with PSD3 and the Payment Services Regulation (PSR) likely set for full implementation sometime in 2027. Its main developments will include more standardized APIs and stronger cybersecurity protection frameworks, expansion of Variable Recurring Payments (VRPs), e.g. electricity consumption bills which are expected to go live soon as well for various utility and financial services payments, e.g. loans, and eIDAS 2.0, which will standardize digital identity and authentication, further securing open banking payments.

At a glance: what expands after open banking

- Savings data sharing

- Loan data sharing

- Investment data sharing

- Insurance data sharing

Key trends shaping the Open banking future in 2026

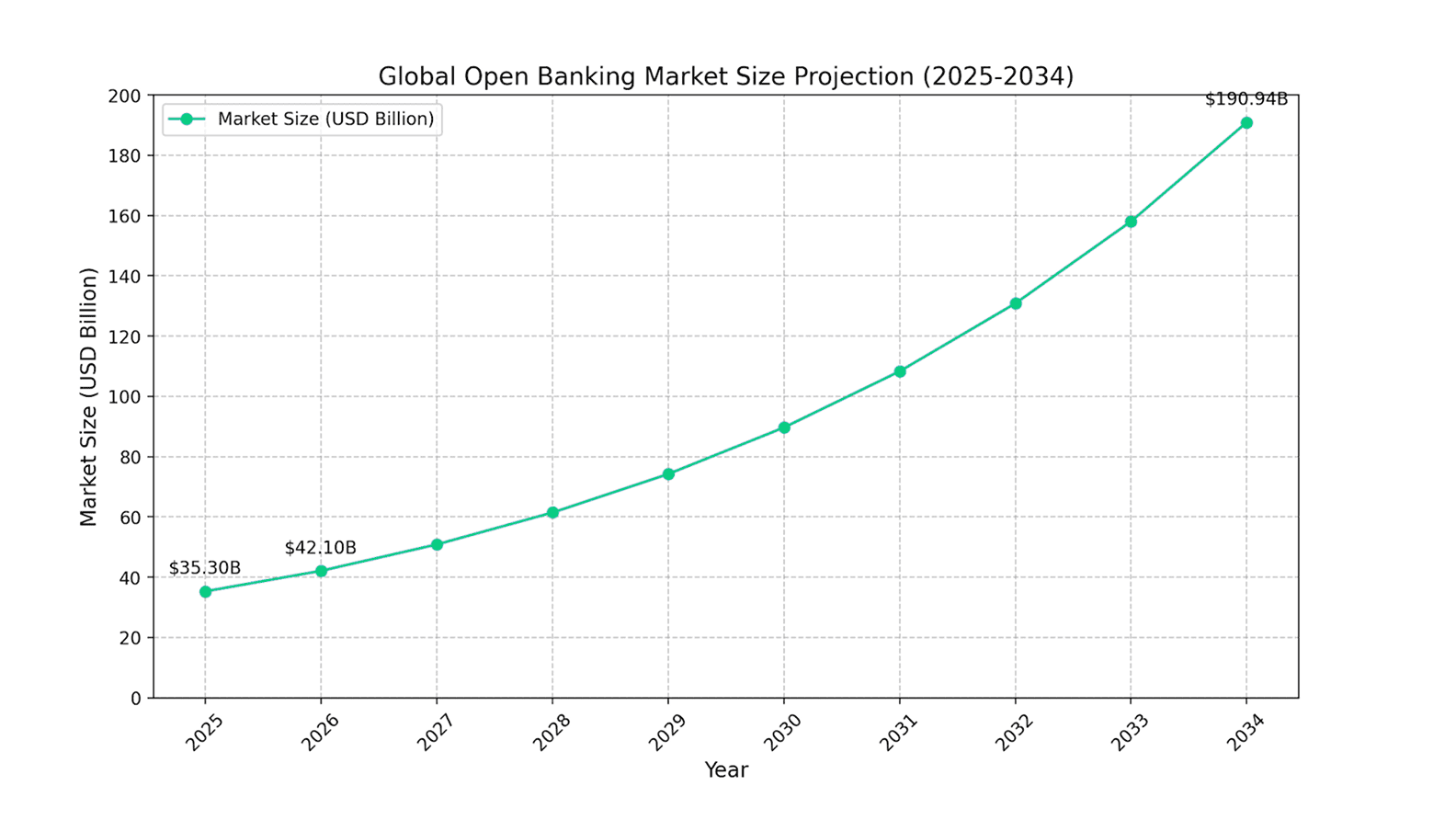

The impact of open banking for fintechs and traditional financial institutions is quite significant. The global open banking market size was valued at USD 35.30 billion in 2025, and is projected to grow from $42.10 billion to $190.94 billion by 2034, with a

CAGR of 20.8% in this period, as shown in the graph below, primarily driven by increased adoption (and now also regulatory mandated by PSD3 in the EU) of open banking APIs for real-time payments, automated budgeting, and tailored loan products (e.g. by offering embedded finance products, where financial services are seamlessly integrated into non-financial platforms, such as Shopify’s capital access for merchants), and AI-driven financial insights, which enable faster, accurate and non-biased credit decisions and personalized financial advice.

Source: Own illustration, based on the Open Banking Market report from Fortune Business Insights (2026)

Real-time payments and liquidity management

In the UK only open banking payments are already growing at around 70% year-on-year,

reaching a record high of 31m open banking payments only in March 2025. This growth is expected to continue, with projections suggesting that open banking has already delivered 8.3bn GBP, and

could generate GBP 43b in annual value for the UK economy at full maturity.

One of the most important underlying trend stemming out of the open banking market growth is the growth of instant payments volumes and real time liquidity management services, where freelancers and small businesses (like myself!) are among the biggest winners of such shift. Platforms like Trovata and Flinks now let users instantly assess cash levels, forecast revenue, and automate expense tracking, reducing manual work substantially and eliminating errors. For a freelancer juggling clients in three countries, this means no more late-night calculation errors or missed tax payments.

Embedded finance

Secondly, it is important to point out the growth of the embedded finance, where financial services are integrated into non-financial platforms. Shopify merchants, for example, can now access capital directly from their dashboard, with AI analysing cash flow to offer tailored loans particularly for them. In the UK, Amazon’s partnership with TrueLayer lets customers pay via bank transfer at checkout, without any card number entries and without any fees, just requiring biometric authentication.

Personalized products and access

Thirdly, financial institutions are already using open banking data to offer hyper-personalized products, with some providers (like Doconomy) helping consumers track and reduce their carbon footprint by analysing spending habits. For underbanked populations, alternative data and new risk models also allow better access to credit, wealth management and insurance, which were traditionally not aimed at wider consumer base.

Regulation and data security

Lastly, stronger regulatory framework introduced by the open banking regulations globally is standardizing data sharing and consent management. For example, as of 1st of April 2026, under the Consumer Financial Protection Bureau’s (CFPB) Open Banking rule in the US, bank account portability became a reality, letting consumers move their financial history between institutions as easy as switching mobile carriers. There, customer data security remains the key, but again the EU, with its PSD3, GDPR and eIDAS 2.0 regulations with encrypted APIs and data privacy rules going well hand-in-hand, leads the pack globally.

Key open banking trends in practical terms

- More real-time payments

- Better liquidity visibility

- More embedded finance options

- More personalized financial products

- Stronger consent and security frameworks

FAQ: Addressing common questions about Open banking

- What is the future of Open banking?

The future of open banking in its core lies in data sharing extending beyond payments to all financial products. By 2027, further interoperability between all stakeholders across the chain, i.e. banks, fintechs, and other third party vendors is expected to become the norm with the UK and EU leading the charge, driven by regulations like PSD3 and evolving frameworks in other countries, like the US and Asian countries.

- How is Open banking changing financial services?

Open banking is enabling

business financial services innovation for example by reducing reliance on outdated legacy system, at least from the user experience perspective, or supporting real-time data sharing and AI-driven insights built on top of it, or by facilitating embedded finance and multi-rail payment systems.

- What does Open banking mean for fintechs?

For fintechs, open banking means access to far broader scope of financial data, enabling them to create hyper-personalized products and services, targeting the right clients with the right products, improving credit scoring, and streamlining overall operations for them and their clients. It may also foster more, in both qualitative and quantitative terms, partnerships with traditional banks, potentially leading to revenue-sharing models and data-as-a-service opportunities.

- How can businesses benefit from Open banking?

Businesses may use open banking to automate financial processes (e.g. reconciliation, payments, tax payments, etc.), enable access to alternative lending and credit options, and naturally enhance user experiences with embedded financial services.

- Is Open banking secure for consumers?

Yes, as much as your data is secure within the bank, it is secure to the same degree if used by open banking products and services when implemented with strong regulatory oversight. The EU’s FiDA and PSD3 frameworks, for example, include robust consent management, fraud protections and standardized APIs to ensure data privacy and cybersecurity.

- What comes after open banking?

What comes after open banking is broader open finance, where data sharing extends beyond payment accounts into savings, loans, investments and insurance. In practical terms, this means the same core idea of secure data portability starts applying to a much wider range of financial products and services for both consumers and businesses.

Summary

The open banking future, or better called already more generically open finance, isn’t just about APIs or regulations. It’s about real people, the freelancer who gets paid instantly, or the small business owner who automates invoicing, or the consumer who compares loan offering across the board in seconds. As APIs, AI, and embedded finance are already converging, businesses, fintechs, and consumers will benefit from more personalized, efficient and more secure financial products and services. The only remaining question is not if, but how quickly businesses and fintechs will adapt to this shift, and very likely those who embrace the open finance today will lead the financial services innovation tomorrow.

Share this article