The EU’s Digital Euro: What It Means for Banks, Fintechs, and Consumers

By

Hamna Zain

09.04.2026

9 min

Something shifted in European payments between last December and now, and most people missed it. The digital euro went from being one of those things policymakers talk about at conferences to something with real timelines, real budgets, and active legislation moving through Brussels. The Council locked in its position in

December 2025. Parliament voted yes in February. EU leaders also pushed last month to get the law finished this year. The ECB is now saying 2029 for launch, which in central bank time means this is actually happening. This article looks at the EU digital euro, why digital euro Europe has become a sovereignty issue, and what digital euro for banks, digital euro for fintechs, and digital euro for consumers could actually mean in practice as Europe moves toward a possible

European digital currency.

I have been watching payment infrastructure projects get announced and quietly die for fifteen years. This one feels different, mostly because nobody is trying to sell it as revolutionary anymore. The pitch is boring: Europe needs payment rails it controls, rails that work across borders, rails that do not depend on three American companies. When central bankers start talking about sovereignty instead of innovation, they are usually serious.

The Dependency Problem Nobody Wants to Say Out Loud

Walk into any shop in Frankfurt or Milan or Amsterdam and watch what happens when someone pays. Visa or Mastercard processes it. Maybe Apple Pay or Google Pay handles the authentication. The hardware might be European, the bank might be European, but the core infrastructure routing that transaction? Not European.This growing dependence on non-European payment providers is a key reason why the digital euro is increasingly framed as a

European payment sovereignty issue.

This bothers regulators more than it bothers consumers, which is probably why the digital euro increasingly framed as a sovereignty issue. The ECB's argument is straightforward: too much of the eurozone's retail payment market relies on non-European payment infrastructure, and domestic alternatives tend to stop at national borders. A Dutch payment app works great in Rotterdam and nowhere in Portugal. A German card scheme is useless in Greece.

| Date | What happens |

|---|---|

| December 2025 | The Council locked in its position |

| February 2026 | Parliament voted yes |

| 2026 | EU leaders pushed to get the law finished this year |

| Mid-2027 | Pilot transactions start mid-2027 |

| 2029 | The ECB is now saying 2029 for launch |

| 2029 | If it works, the commercial phase starts in 2029 |

The proposal creates a public digital payment system backed by the Eurosystem with legal-tender status. Merchants accepting digital payments would have to accept it. Distribution would run through banks and regulated payment firms. It would sit alongside cash, not replace it, and the regulation explicitly protects access to physical cash while introducing a digital public payment option.

What makes this different from the dozen other European payment initiatives that went nowhere is that this one has enforceable legal and regulatory backing. Legal-tender status means merchants cannot refuse it the way they can refuse proprietary wallets or loyalty schemes. Mandatory acceptance means instant network effects and widespread adoption from day one, assuming the law passes.

Why Banks Went From "Absolutely Not" to "Let's Talk Terms"

The banking industry spent the first two years of digital euro discussions explaining why it would disrupt the traditional banking model and potentially destabilize the financial system. Deposits would flee to the central bank. The business model would collapse. Credit would dry up. Small banks would die. That is the core anxiety behind the impact of the digital euro on banks, and it has shaped almost every serious lobbying fight around the project.

The

ECB listened, apparently, because the current design addresses most of that. Holdings capped to limit deposit outflows and protect financial stability at a level that has not been finalized but will be low enough that nobody is parking their savings there. No interest. Wallets can be linked to commercial bank accounts through a “reverse waterfall” mechanism for excess balances. The message to banks is: we are not competing for deposits, we are giving you infrastructure.

But infrastructure costs money.

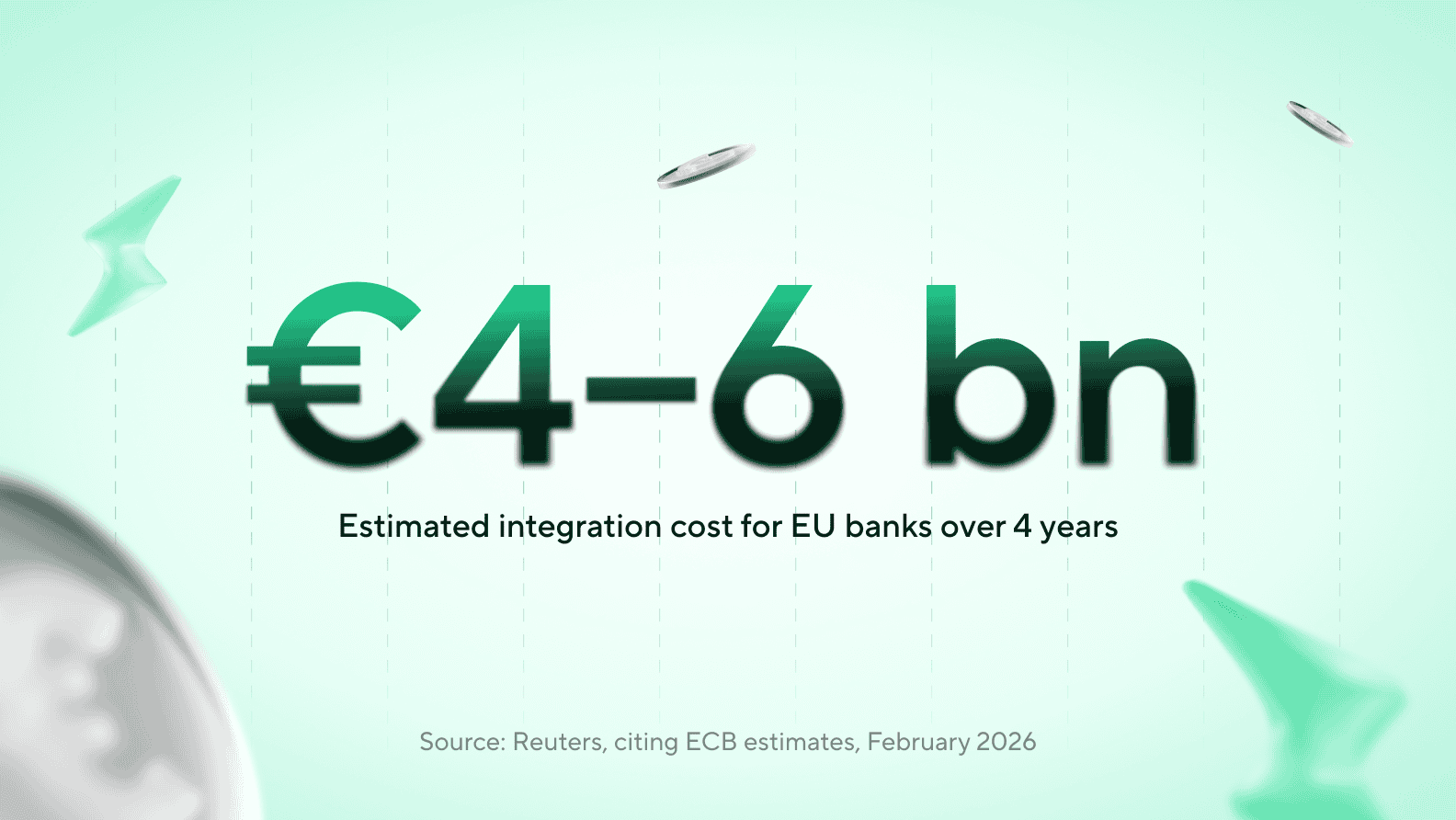

Reuters reported the ECB's own estimate in February: somewhere between €4 billion and €6 billion for EU banks over four years to implement the digital euro infrastructure across the eurozone. . That is not a trivial number, and it does not include ongoing operational and regulatory compliance costs, or the compliance work that always ends up being more complicated than the initial estimate.

The trade-off, according to the ECB, is that banks keep the customer relationship, earn merchant fees, and reduce reliance on international card schemes such as Visa and Mastercard. Whether that math works depends entirely on the fee structure, which is still being negotiated. One senior banker told me off the record that the project is "expensive but survivable if we actually get compensated for distribution." Translation: show us the revenue model or we are going to lobby this into oblivion.

What shifted the conversation from outright opposition to negotiation was the realization that the digital euro is probably happening whether banks like it or not. Fighting it became less productive than shaping it. The current design keeps payment service providers at the center of distribution and gives them responsibility for customer-facing services, which is about as good an outcome as the industry could have hoped for.

The Fintech Opportunity (If You Build the Right Thing)

Fintech companies are not going to issue digital euros. That stays with the ECB. But the innovation platform the central bank ran last year with nearly 70 participants showed where the real opportunity sits: on top of the infrastructure, not underneath it. That is the real opening in digital euro for fintechs.

The use cases that came out of that work were practical. Conditional payments that trigger automatically when something happens. Refunds that process without manual intervention. Digital receipts integrated into the payment. Mobility payments for trains and buses across borders. Wallet designs that actually work for people with visual impairments or limited digital literacy.

A payments executive I know put it well: "We are not here to be a bank. We are here to make paying for things less annoying than it is now." That is the strategic opening. The digital euro becomes the commodity layer, the boring infrastructure everyone uses. The product differentiation happens in the interface, the fraud controls, the merchant tools, the loyalty integration, the embedded payment logic.

For fintechs that have been building point solutions in fragmented national markets, this is a chance to scale across borders without rebuilding infrastructure for every country. Right now, a payment product that works seamlessly from Lisbon to Helsinki means integrating with multiple national systems and navigating inconsistent standards. A harmonized digital euro rail could eliminate a lot of that friction.

The winners will be firms that build better onboarding, better checkout experiences, better analytics for merchants, better accessibility features. The losers will be anyone who just repackages the same functionality as their competitors but with different branding.

What Consumers Actually Get (And What They Don't)

The consumer proposition is deliberately unsexy. This is not an investment. Holdings are capped. No interest. The whole design points toward spending, not saving. That is what digital euro for consumers looks like in its most basic form.

| What the digital euro is | What it is not |

|---|---|

| A public digital payment option | Not a cryptocurrency |

| Designed for everyday transactions | Not an investment |

| Meant to complement physical cash | Not a replacement for physical cash |

| Backed by the Eurosystem | Not privately issued |

| Built for spending | Not designed for saving |

| Subject to holding caps | Not interest-bearing |

What you would get: free basic use, instant payments, acceptance across the eurozone anywhere that takes digital payments, offline functionality that works without internet, and privacy protections for offline transactions that mirror cash. The Eurosystem would not see details of offline payments.

That privacy piece is important because one of the ECB's biggest communication challenges is convincing people this is not a surveillance tool. A lot of consumers hear "central bank digital currency" and think the government will track every coffee they buy. The offline payment design addresses that directly. Use it like cash in situations where you do not need connectivity, and the transaction is invisible to the central bank.

The accessibility requirements go beyond the usual regulatory checkbox. Support for people with disabilities, people with low digital skills, people without bank accounts. How well that gets implemented will depend on the banks and payment providers doing the distribution, but the legal requirement is there in the proposal.

You would not download a "digital euro app." You would access it through your existing bank or a payment provider you choose. The digital euro itself is just the money. The interface is someone else's problem, which is probably the smartest design decision the ECB made.

Stakeholder Impact Summary

| Who | What They Get | What It Costs Them | The Real Question |

|---|---|---|---|

| Banks | Keep customer relationships, earn merchant fees, avoid some card network costs | €4–6bn implementation over four years, ongoing compliance burden | Is the fee structure worth the integration cost? |

| Fintechs | Pan-European payment rail, harmonized standards, cross-border scale | Must compete on product quality instead of owning the stack | Can we build a better experience than banks? |

| Consumers | Free basic use, broader acceptance, offline payments, privacy protections | Capped holdings, no interest, no investment upside | Is this actually more useful than what I use now? |

The Risks That Could Still Kill This

Political timing is the biggest variable. The ECB's schedule assumes the regulation passes in 2026. If that slips, everything slides. Even if the law clears on time, the institution is planning two more years of preparation before issuance, with

pilot transactions starting mid-2027.

There is also a messaging problem the ECB has not solved. When people hear "CBDC," they think surveillance, programmable money, government control. The central bank keeps saying the digital euro would not be programmable in the sense of restricting how you spend it. Conditional payments would exist, but those would be services from private providers, not controls from the Eurosystem.

Whether that nuance lands with the public is doubtful. The ECB is not known for clear communication, and the gap between "the central bank cannot see your offline payments" and "the central bank is monitoring everything" is small enough that it will get lost in translation.

The institution has been explicit: the Eurosystem would not directly identify users from their payments, offline transactions would have cash-like privacy, the system would not be programmable money. But turning technical specifications into public trust is harder than building the architecture.

What 2027 Actually Looks Like

If the regulation passes this year, 2027 is when policy becomes code. The

pilot phase tests whether the technical design works and whether the user experience is good enough for real adoption. Expect small-scale boring tests: payments between wallets in controlled environments, maybe some merchant pilots.

If it works, the commercial phase starts in 2029. Banks decide how hard to push it. Fintechs decide whether to build on it or ignore it. Consumers decide whether it solves a problem they have or just adds another option they do not need.

Adoption will be uneven. Some markets will move faster because their domestic infrastructure is weak or cross-border payments matter more. Some demographics will adopt quickly because they are already comfortable with digital payments. Some merchants will integrate fast because they see cost savings. Others will resist.

What seems unlikely is that this gets built and nobody uses it. Too much political capital is invested. Too many institutions are committed. The underlying problem – fragmented infrastructure, dependence on non-European providers, barriers to cross-border commerce – is real enough that demand exists.

The question is not whether Europe wants this. The question is who builds on it first and builds well enough that people actually use it. And for readers asking when will the digital euro launch, the ECB's current answer is 2029, assuming the legislation passes in 2026 and the pilot starts in the second half of 2027.

FAQ

What is the EU’s digital euro?

In plain terms, what is the EU digital euro? A digital form of central bank money for retail payments, issued by the Eurosystem, designed to complement physical cash. You would access it through banks or payment providers and use it for everyday transactions across the euro area.

How is the digital euro different from cryptocurrency?

Put another way, is the digital euro the same as cryptocurrency? No. Crypto is privately issued and its value fluctuates based on market demand. The digital euro would be public money backed by the ECB, designed to stay equal to one euro. It is infrastructure.

What could the digital euro mean for banks?

This is really the question of how will the digital euro affect banks. They stay in distribution, keep customer relationships, get a new payment rail. But they also face €4 to 6 billion in integration costs and need to modernize their payments business. The revenue model is still being negotiated.

How might fintech companies benefit from the digital euro?

In practical terms, what does the digital euro mean for fintechs? Access to a Europe-wide standard they can build on top of. Think checkout tools, refund automation, merchant analytics, fraud detection. The opportunity is in better user experience and cross-border scale, not in issuing money.

What does the digital euro mean for consumers in Europe?

This is the everyday-use question: how will consumers use the digital euro? A wallet or card to pay in stores, online, person to person. Works offline in some situations. Basic services free. Designed for spending, not saving.

Will the digital euro change how euro payments work?

Potentially, yes. It would create a public payment option with legal-tender status, wider mandatory acceptance, and a more harmonized cross-border base layer for euro payments. If it works as intended, it changes less about the idea of paying and more about who controls the rails underneath.

Summary

The digital euro is no longer just a policy concept floating around Brussels. It has dates, legislative momentum, cost estimates, and a technical roadmap behind it.

For banks, it looks expensive but potentially manageable. For fintechs, it looks like a rare chance to build across borders on a shared public shared pan-European payment infrastructure. For consumers, it looks less like a revolution than a state-backed digital payment solution designed for everyday transactions , not savings. Europe is not building this because it is fashionable. Europe is building it because control over payments infrastructure has stopped looking optional.

Share this article