Why Does My Card Get Declined at Hotels and Car Rentals? (And How to Fix It)

By

Emma Carter

23.03.2026

12 min

You've checked your balance. There's plenty of money. You hand over the card at the rental desk or hotel check-in — and it gets declined anyway.

It happens to a lot of people, and the frustrating part is that it has almost nothing to do with whether you actually have enough funds. It's about a mechanic called a pre-authorization hold, and how your card's underlying type interacts with it. Once you understand the logic, the fix is usually simple — but you need to know what's actually happening first.

This guide covers why declines happen, which card types are most affected, what "credit-grade" actually means and why it matters, and what you can do before your next trip so this isn't a problem.

What hotels and car rentals are actually doing when they "charge" your card at check-in

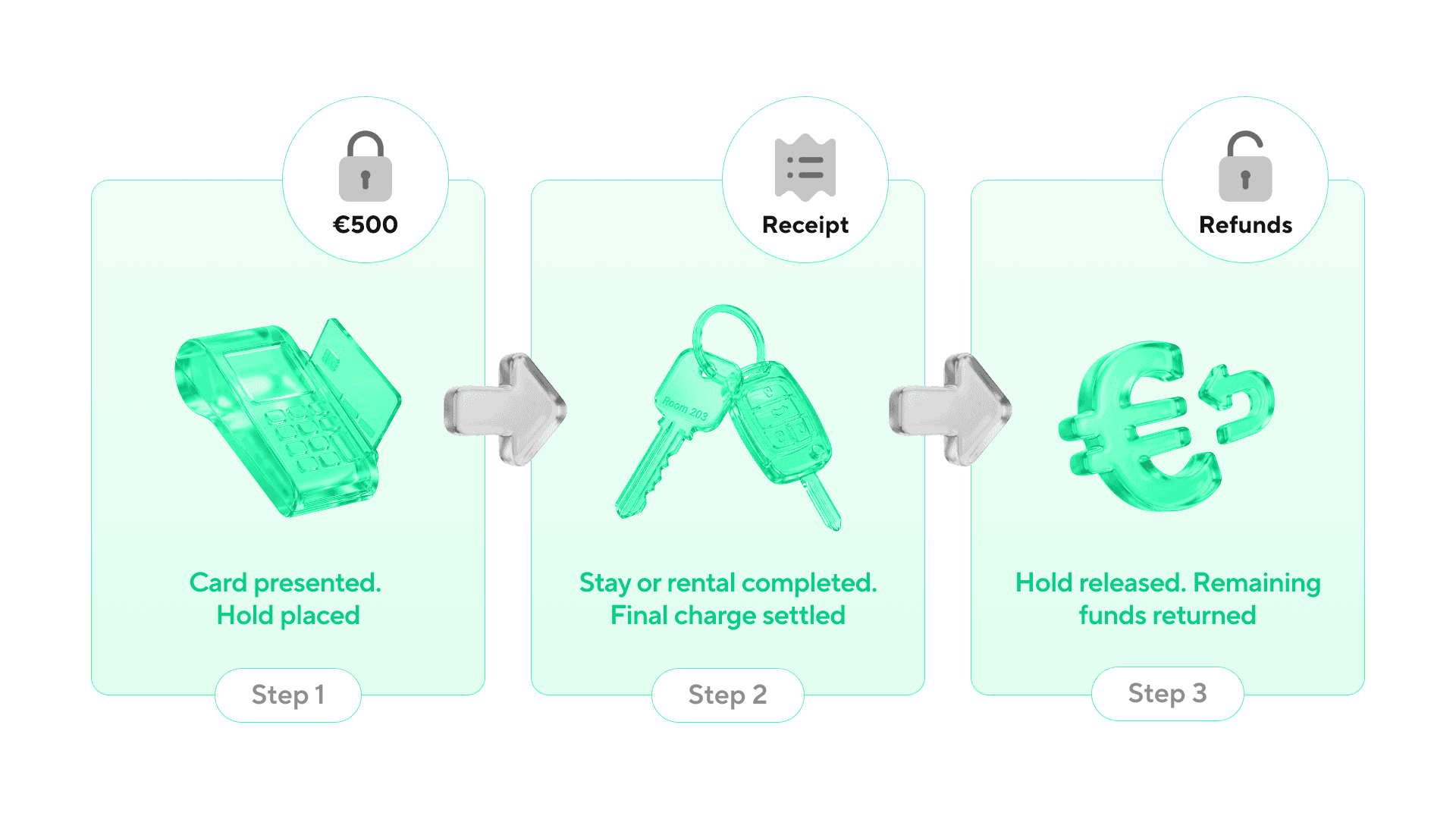

Here's the thing most people don't realize: when you hand over your card at a hotel or car rental desk, they're not charging you for your stay or rental yet. They're placing a temporary hold — also called a pre-authorization — on your card.

The hold works like this: the hotel or rental company sends your card issuer an authorization request for an estimated amount. Your issuer freezes those funds. The money doesn't go anywhere, but it's no longer available for you to spend. When you check out or return the car, the actual charge settles and the hold is released.

Why do they do this? Because at check-in, the final bill is unknown. You might order room service. You might return the car with an empty tank. You might scratch the bumper. The hold is their insurance that funds will be there when the final amount is calculated.

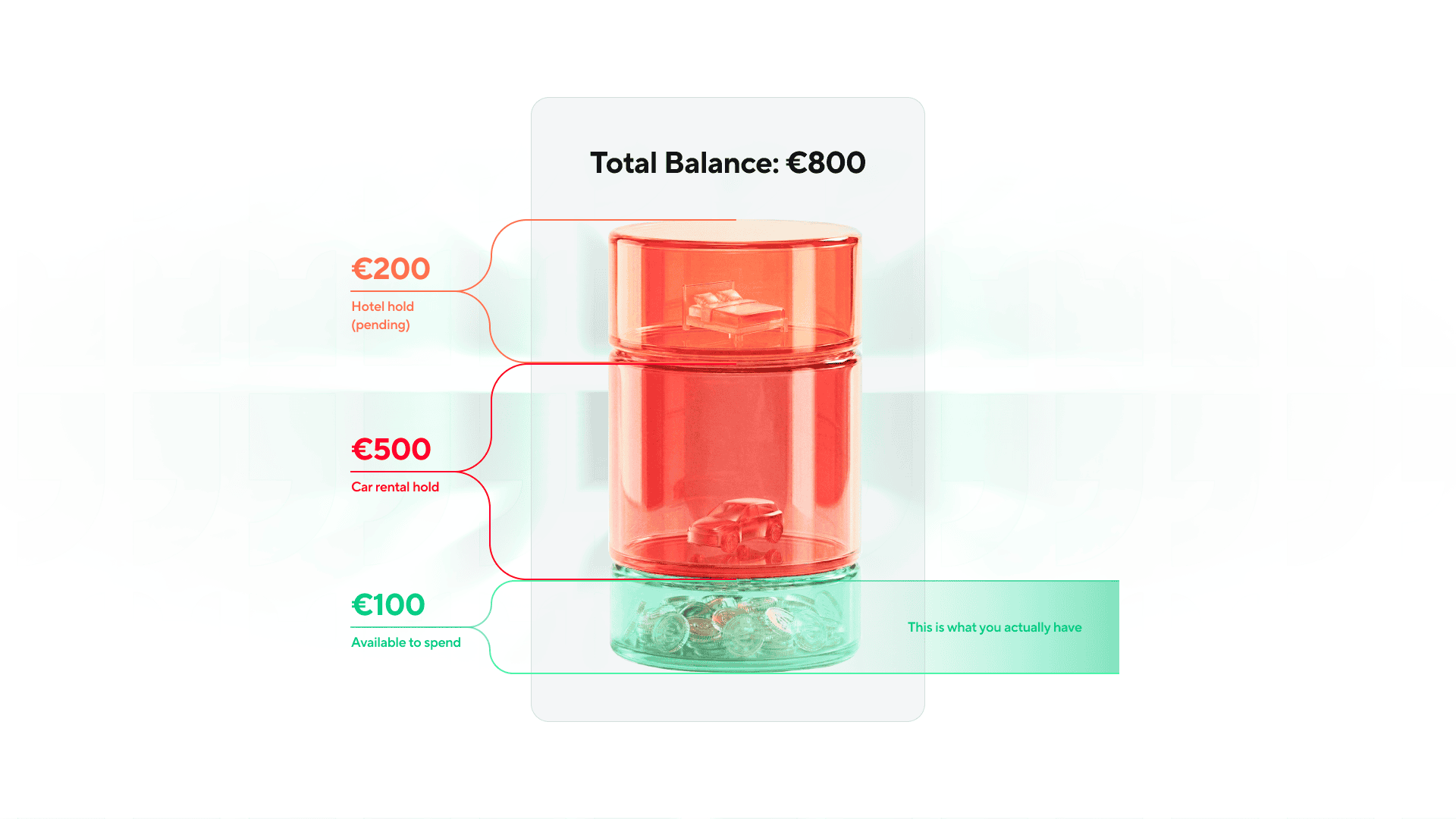

The hold amounts are bigger than most people expect:

| Merchant type | Typical hold amount (Europe) |

|---|---|

| Budget hotel (1–2 nights) | €50–€150 on top of room rate |

| 4-star hotel | €200–€500 |

| Car rental (economy class) | €200–€400 |

| Car rental (premium/SUV) | €500–€1,500 |

| Car rental at airport | Often higher than city locations |

And here's the key detail: the hold sits on your card for days after you check out or return the car. Usually 3–7 business days, sometimes longer depending on your card issuer. If you're traveling and using the same card at multiple hotels in a row, those holds stack up.

Car rental industry data confirms what travelers experience anecdotally: many fintech-issued cards are treated by merchant payment systems as prepaid or "cash-equivalent," regardless of the balance behind them. When a terminal flags a card this way, some rental desks will refuse it automatically for deposit holds — even though the same card could be used to pay the final bill once the car is returned. The distinction matters: it's not that your money isn't good enough, it's that the card's technical classification doesn't match what the merchant's system requires for a pre-authorization. If your card is positioned as a travel-friendly, low-fee alternative to traditional cards, don't assume that extends to hotel deposits and rental security holds. These are the exact transactions where card classification is enforced most strictly.

So why does the card actually get declined?

There are a few different reasons, and they're worth separating because the fix is different for each.

Reason 1: Not enough available balance — even if the total looks fine

This is the most common cause, and it trips people up because the math seems wrong.

Say you have €800 in your account and you're booking a €300 car rental. That should be fine, right? Except the rental desk places a €500 hold for the security deposit — and if your previous hotel already placed a €200 hold that hasn't cleared yet, your actual available balance at that moment is €800 − €200 = €600. The rental hold of €500 fits, but just barely. Add any fraud buffer the card issuer runs, and you might get a decline.

The rule of thumb: always have significantly more available than the total of your expected holds, combined. When traveling, assume at least €500–€800 in headroom above what you plan to spend.

Reason 2: Your card type is being rejected outright

This is where it gets more technical — and where the type of card you carry makes a real difference.

When a card terminal processes a transaction, the first thing it reads is the BIN — the Bank Identification Number, which is the first 6–8 digits of your card number. This tells the system instantly whether your card is classified as credit, debit, or prepaid.

Many hotels and car rental companies have a clear policy: prepaid cards are not accepted for security deposits. Full stop. Not because of your balance, but because of the card classification itself. Some also reject standard debit cards and require a credit card specifically.

The reasoning: a credit card's authorization process is more predictable for the merchant. They know funds are guaranteed by the issuing bank up to your credit limit. With a prepaid card, the issuer has less standardized infrastructure for authorization holds, and the merchant has less confidence the hold will behave correctly when they come to settle.

This is why a lot of people who have moved to fintech cards — which are often classified as prepaid — run into this problem even when they have a perfectly healthy balance.

This isn't a theoretical problem. Travel forums and fintech community boards are full of stories from people who were turned away at car rental desks — sometimes multiple times on the same trip — because their card was flagged as prepaid. In many cases, these were cards marketed specifically as travel cards, with competitive exchange rates and no foreign transaction fees. The travelers had more than enough funds. The card worked perfectly at restaurants, shops, and ATMs. But at the rental counter, the terminal read the BIN, classified the card as prepaid, and the agent said: "Sorry, we need a credit card." Some users report that even when their fintech provider had upgraded them to an actual credit product, the rental desk still refused the card because the company behind it wasn't recognized as a traditional institution. The card itself was fine — but the system didn't treat it that way.

Reason 3: Your issuer's fraud systems flagged it

Large pre-authorization requests look different to fraud detection systems than regular purchases. A €400 hold at an unfamiliar airport in a foreign country, placed by a merchant category your card has never seen before — that's exactly the kind of transaction that triggers an automatic block, even if everything is legitimate.

Your card issuer may simply put a stop on it pending verification, and the rental desk just sees "declined" with no further information.

Reason 4: Name or document mismatch

Many rental companies require that the card used for the deposit matches the main driver's name exactly. If the booking is in one name and the card is in another — even a spouse or partner — the desk can refuse it. This is a policy-level refusal, not a card-level one, but it produces the same result at the counter.

The credit BIN difference: why some fintech cards work where others don't

Here's something that trips up a lot of users of modern fintech cards.

Not all fintech cards are created equal at a hotel or rental desk. The difference comes down to how the card is classified at the network level — that BIN again.

A prepaid BIN tells the merchant's system: "this is a prepaid card." Many rental and hotel systems will automatically reject this, regardless of balance or issuer.

A credit BIN — or what's sometimes called a credit-grade card — tells the system: "this is a credit-type card." It gets treated the same as a credit card in terms of authorization handling. The merchant's system accepts the hold, processes it correctly, and you get the car keys.

This matters specifically for people using e-money accounts and fintech payment cards. A lot of these cards run on prepaid BINs, which is part of why users report getting declined at rental counters even though they use the same card everywhere else without issue.

The

Blackcat payment card that you can check on blackcat.app has a credit-grade BIN, so even though it does not offer any credit products or overdraft, it is widely accepted for hotel bookings, car rentals, and deposit holds that reject standard prepaid cards.

What to actually do before your trip

Most of this is preventable with a bit of preparation.

Check what card type you're carrying. If you're not sure whether your fintech card runs on a prepaid or credit BIN, check the card's documentation or ask support. It matters.

Notify your card issuer before travel. Most issuers still benefit from advance notice of travel, especially for large authorization requests in foreign countries. Even if your issuer says "we don't need travel notices anymore," a quick in-app notification or a call takes two minutes and can prevent a fraud block at the worst moment.

Check your available balance, not your total balance. Before you go to the rental desk, calculate: total balance, minus any pending holds, minus what you're planning to spend. That's your actual available amount. Make sure the rental deposit comfortably fits within that.

Carry a backup. Even if your main card should work, having a second card — ideally a different type from a different issuer — is the practical solution when you're at an airport counter at 11pm and the desk closes in ten minutes.

Know the hold release timeline. If you're doing multiple legs of a trip with hotels, the hold from your first hotel may still be active when you check into the second. Budget for this. Holds typically take 3–7 business days to release, sometimes longer.

A quick reference: what usually works where

| Scenario | Works reliably | Works sometimes | Often rejected |

|---|---|---|---|

| Hotel check-in (European 3–4 star) | Credit card, credit-grade payment card | Standard debit card | Prepaid card |

| Car rental (standard) | Credit card, credit-grade payment card | Bank debit card | Prepaid card, virtual-only card |

| Car rental at major airports | Credit card, credit-grade payment card | Bank debit card (verify in advance) | Prepaid, virtual, non-embossed |

| Car rental (premium/luxury class) | Credit card | Credit-grade payment card (verify) | Debit, prepaid |

| Airbnb / online hotel booking | Most card types | — | Some prepaid |

The short version

Your card gets declined at hotels and car rentals for one of four reasons: not enough available balance once holds are stacked, a card type that's rejected outright (usually prepaid), a fraud flag from an unusual large authorization, or a name mismatch at the desk.

The most preventable cause — and the one that catches the most people by surprise — is carrying a prepaid-BIN card and running into a merchant policy that flat-out doesn't accept them for security deposits. Switching to a card with a credit-grade BIN solves this entirely, without needing an actual credit card. See how the

Blackcat payment card handles this.

Before your next trip: check your card type, check your available balance with holds factored in, notify your issuer, and bring a backup. That combination handles the vast majority of scenarios.

FAQ:

Why does my card get declined at car rental even though I have enough money?

Most likely it's a card type issue, not a balance issue. Car rental desks place a security deposit hold that can be €200–€1,500, and many locations flat-out reject prepaid cards for this — regardless of your balance. If your fintech card runs on a prepaid BIN, it will be declined even with plenty of funds available. Check whether your card has a credit-grade BIN; if not, bring a backup.

How long does a hotel hold stay on my card?

Usually 3–7 business days after checkout, but it depends on your card issuer. Some release it faster, some take up to 10 days. If you're moving between hotels on a trip, those holds can stack — so factor in the full amount of all active holds when checking your available balance.

Can I use a virtual card at a hotel or car rental?

For online bookings, usually yes. At the physical desk, many car rental companies require a physical card with an embossed name for the security deposit. Virtual-only cards are often rejected at the counter even if they work fine online.

What's the difference between a prepaid card and a credit-grade card?

A prepaid card is classified at the network level as a stored-value card — you load funds onto it and spend what's there. A credit-grade card uses a credit BIN, meaning the card network treats it like a credit card in terms of how authorization holds are processed. The key point: it doesn't mean you're borrowing money. The Blackcat payment card is a payment card linked to your account balance, not a credit product — but its credit-grade BIN means it's accepted where prepaid cards aren't.

My card worked at a hotel last year but got declined this time. Why?

A few possible reasons: the hotel may have tightened its card acceptance policy, your card issuer may have flagged the transaction as unusual (especially if you're traveling abroad), or you may have had less available balance than expected due to stacked holds from earlier in your trip. It's worth calling your card issuer immediately — they can often clear a fraud block on the spot and let you retry.

Share this article